WealthBar is a unique offering in the digital investment management space in Canada. Yes, they are often called ‘Robo Advisors’ but that is not necessarily an accurate moniker and it brings up images of robots as advisors, and a lack of human contact. That’s certainly not the case. These investment companies simply use technology as an enabler to enhance the comprehensive (and very human) investment offerings. And of course the technology allows these firms to lower fees by some 70%, 80%, 90% or more compared to traditional funds and advice.

Please note, WealthBar is now CI Direct Investing. Nothing has changed but the name. CI took full ownership in August of 2020.

The technology can certainly enable you to do everything online, from on boarding to completing your investor profile to obtaining your well-diversified investment portfolio. You can choose the digital route from start to finish, or you can access the help of advisors and customer support. Your experience at WealthBar would start with a review of your Plan by your dedicated licensed advisor. There are also ongoing annual reviews with your advisor. There are financial planning tools available that can help keep you on track.

Humans when you want them, digital when you don’t.

In the end the technology will also enable those incredible savings on fees. Those lower fees might be the main benefit, allowing you to keep more monies in your portfolio pocket.

WealthBar is unique in that it offers access to Private Investment Portfolios featuring alternative investments. While the other digital wealth managers create portfolios using popular exchange traded funds, WealthBar also offers access to investments that are usually reserved for the rich. Tea Nicola is the CEO of WealthBar. Tea and husband Chris Nicola co-founded WealthBar. Chris’s father, John Nicola, is the chairman and CEO of Nicola Wealth.

Private Investment Pools simply collect funds from a pool of investors, they then have the freedom to venture out and invest directly in any investment of choice. For example they may go out and purchase or fund a building or buildings (real estate investments) or a bundle of mortgages or use options strategies to create greater income. The goal is to create a more balanced approach to investing. The pooled funds can add more consistent income and lessen risk or volatility. Many of the assets tend to not fluctuate in value as much as traditional stocks or stock funds, or typical Balanced Portfolios.

Below we see the performance of a Nicola Wealth Pooled Fund Portfolio approach through the last recession – the Financial Crisis. The grey line represents the Canadian Stock Market, the green line represents a Nicola Wealth Portfolio. We see that lower risk portfolio greatly outperform the Canadian stock market through (and beyond) that major market correction. That portfolio also held up much better than traditional Balanced Portfolios.

Below we see the performance of a Nicola Wealth Pooled Fund Portfolio approach through the last recession – the Financial Crisis. The grey line represents the Canadian Stock Market, the green line represents a Nicola Wealth Portfolio. We see that lower risk portfolio greatly outperform the Canadian stock market through (and beyond) that major market correction. That portfolio also held up much better than traditional Balanced Portfolios.

The pooled fund approach seeks better risk-adjusted returns. Mission accomplished through the last recession.

The Private Portfolios are offered at 3 risk levels.

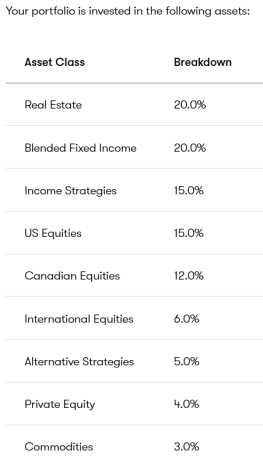

The portfolios are well diversified across geographies and asset classes including Canadian, US and International stocks. Here’s an example using the Balanced model. The Private Fund MERs are higher than traditional ETF portfolios.

MERs by Private Portfolio.

- Safety Private Portfolio 1.0%

- Balanced Private Portfolio 1.56%

- Aggressive Private Portfolio 1.37%

But we can see from the performance chart it was money well spent. While fees are very important when comparing a similar investment approach it is not as important (or important at all) when one has access to a unique investment approach.

How and when do you choose the option of typical core portfolio or Private Funds?

You will be offered the Nicola Wealth option after you complete your online investor profile. WealthBar clients can invest all of their funds, or a portion of their funds in the Private Portfolios.

Of course at WealthBar you can still go that traditional ETF route.

They have their own unique approach with respect to ETF Model Portfolio construction.

Here’s an example – using the Growth Portfolio. WealthBar will access ETFs from a broad range of providers. You’ll see the use of high yield bonds, covered call funds and preferred shares. Even when they’re ETF’n these folks like their income and that effect upon the portfolio returns and risk. BMO is a great source and resource for more income oriented assets.

How much does it cost?

The fees include transaction costs, advice and administrative costs. The fee bands –

- $1,000 – $149,999 = 0.60%

- $150,000 – $499,99 = 0.40%

- $500,000 and above = 0.35%

You can use the this pricing page to determine the dollar value that you would pay in fees based on a specific investment amount. At $100,000 you would pay $50 per month in fees. With a traditional mutual fund you would pay $183 or more per month.

And of course there are also the MERs of the portfolios.

And once again it is not always about the fees. A unique investment approach can compensate for slightly higher fees. When I benchmark the WealthBar ETF portfolios I find that the results are very good. Even on their site, you’ll see them do a head-to-head performance comparison against a well-known ‘competitor’. You might guess who comes out ahead. Robo wars.

And wait, there’s more! You can even add a very well-performing Clean-tech component to your portfolio.

Step up to the WealthBar for Private Investments Pools.

Once again, each of the Canadians Robo/Digital Wealth Managers is unique. And that’s a good thing. Investors should seek out and find the investment firm and approach that is right for their situation and needs. WealthBar is the only ‘Robo’ to offer these investments normally reserved for ‘the rich’. You may find this very attractive if you’re more concerned with investment risks; or you may simply seek better risk adjusted returns. Retirees might also have a look at WealthBar as lower volatility and regular investment income can be a wonderful benefit with respect to creating durable and generous retirement income.

As with other digital firms, portfolios are insured to $1,000,000.

Thanks for reading, I will be back with a more detailed look at the core ETF portfolios and their SRI Socially Responsible Investing clean tech component.

If you feel that WealthBar is right for you, and when you sign up through this link, as a Cut The Crap Investing reader you will have the first $15,000 managed for free for one year.

While I do not accept monies for feature blogs please click here for more about Dale and ‘how I might get paid’ disclosures.

Thanks for reading. Kindly hit those share buttons for Twitter, Facebook and LinkedIn and more.

For any questions on this review, please use that contact form, or leave a comment on this post.

Dale

Thanks so much for the article on Wealthbar. It’s a great affirmation of my decision to go with them a couple years ago. I’m currently an ETF client with WB and from my conversation with one of their financial planners am considering moving some over to the Nicola Core portfolio. Your blog has been very helpful in moving forward on that decision and explaining why fees aren’t the be all and end all when looking at the end game.

Thanks Lora, I do think WealthBar is an incredible option. And those Nicola wealth private pool funds are a major differentiator. I am working on a post for private pool funds and with a look at the offerings and options for WealthBar clients.

And the advice can be quite robust as well as WealthBar. I imagine you’ve had a good experience on that front?

Thanks for your comment. I am glad that you found this post, and that you found WealthBar.

Dale

I realize this is an older post. It doesn’t seem as though the Private Investment Pools are offered anymore which is a great shame.

Thanks, I certainly need to update this post.

Dale