Creating a retirement portfolio with Exchange Traded Funds (ETFs) is easy.

Creating a retirement portfolio with ETFs is a challenge.

Both of the above statements is true. Building a retirement portfolio is quite simple, just as building wealth in the accumulation stage is quite simple. And if you’re a self-directed investor using ETFs you’re likely keeping your fees at a rock-bottom .10-25% area. That is one of the most important considerations.

2% for you and 2.5% for your advisor and mutual fund company?

If you’re handing over 2%-2.5% annually in various fees you can guess who’s retiring comfortably, and you can guess who’s retiring early. So congratulations, as a self-directed investor you’re keeping the majority of your retirement monies in your pocket.

But there are other pockets that we need to consider; the pockets of the various tax collectors in Canada, the US and around the world where you might hold your investments. We also want to consider the pockets of your discount broker who might charge you currency conversion charges when you take monies out of your US holdings and convert those asset to Canadians dollars.

Know what goes where.

As much as determining what type of ETF assets to hold and deciding upon your overall portfolio asset allocation we also need to know that goes where with respect to your RRSP, TFSA and Non Registered accounts.

Keep in mind that I have never been a licensed tax professional. It may be more than wise to find a fee-for-service advisor than can help you with the optimal mix of assets, situated in ‘the right place’. They can also help you find the most beneficial order of harvesting your RRSP vs TFSA vs Taxable vs Pension income(s). These decisions could enable considerably greater income and more reliable income over your lifetime.

There are a lot of moving parts when it comes to retirement funding.

Is my Couch Potato Core ETF Portfolio OK for Retirement?

Here’s the good news on the retirement front for ETFers; basic and sensible core balanced portfolios can work wonders in retirement.

We do not need to build an income intensive portfolio. We don’t have to ‘live off of the dividends’.

Your level of retirement income comes down to 2 factors – the growth of the portfolio and the risk level of the portfolio. In retirement the amount or percentage that you can remove to spend from your portfolio is mostly determined by the growth rate of your portfolio. If you’re portfolio is making 7% per year after fees, well you can spend 7% per year and maintain your portfolio value. Of course that tax man is going to get his cut on RRSP and RRIF and LIF withdrawals. Remember, every penny removed for spending is taxed as income. You’re also going to pay taxes on investment income and capital gains realized in taxable accounts.

Total return is totally fine.

Total return ETFs are more than fine, and in fact they might end up being more tax efficient in the end. Again you’re success level and spend rate will come down to portfolio growth and managing the sequence of returns risk.

The risks are different in retirement.

In the accumulation stage market corrections did not historically present long-term risk, as markets have historically always recovered to deliver new highs and renewed portfolio growth. In retirement a severe stock market correction could impair retirement, permanently. Selling assets continually when the market is down kills the cow. You’re owning less of the companies. You’ve had to sell large portions of your shares to fund retirement; you’re decreasing your ownership of those companies and profit centres.

Manage the portfolio risks in retirement

That’s why it is wise to hold a Balanced Portfolio of some sort that includes bonds that work as shock absorbers in market corrections. Not only that the bonds have the potential to go up in price when those stocks get hit – there’s that inverse relationship to stocks. You can sell more bonds, meaning you can sell less of those profit centres known as stocks.

Here’s one of my favourite charts of all-time courtesy of Portfolio Visualizer.

Portfolio 1 is the S&P 500 (US Market)

Portfolio 2 is TLT – (US Long Term Treasuries)

We see that wonderful inverse relationship. Of course past performance does not guarantee future returns or future performance characteristics. That said, bonds have been there to do their thing in every recession. That is government treasuries (especially longer dated) have gone up when stocks went down. I like the odds of a repeat in a major market correction.

To get enough growth out of your portfolio with enough risk management you might consider what I’d suggest is the sweet spot for retirees as 40% stocks to 80% stocks. Of course you have to invest within your risk tolerance level. I’d suggest that your tolerance for risk is more likely to decline in your retirement years.

A Sensible Globally Diversified Balanced ETF Portfolio Should Work Well

Now keep in mind that we do need markets to cooperate over the longer term for any approach to ‘work well’. I’m simply suggesting that you might not need to collapse your wonderful and simple couch potato portfolio to go chase dividends and higher yield bonds and more exotic higher yielding ETFs.

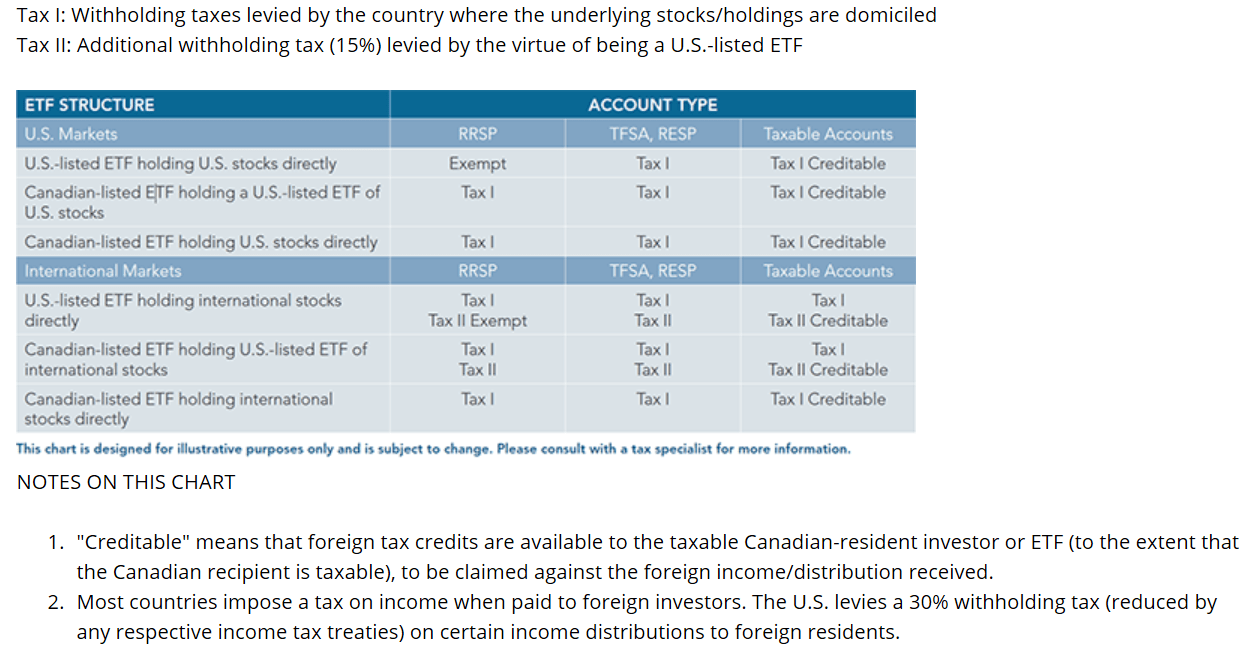

But then there’s that issue of what goes where.

To avoid taxation or to have the ability to recoup US withholding taxes on US Dividends you would be best served to hold those ETFs in your RRSP or Non Registered plan types to take advantage of the tax treaty between the US and Canada for certain registered accounts. With Non Registered Accounts you can apply for the tax credit to recoup those taxes paid.

And on that we do need to hold US listed ETFs to qualify. The wrapped ETFs that hold US ETFs in a Canadian dollar fund of funds such as VXC or XAW or XUU would give up those withholding taxes on US Dividends. We are better off with a direct US dollar IVV or total market VTI as examples.

Avoid currency conversion charges

You’ll also have to read up Norbert’s Gambit to avoid currency conversion charges.

If you have large US assets in US dollar funds or stocks you might want to be careful as the IRS may come looking for you. Read up on that subject or nuance. For taxable monies you can also take advantage of The Canadian Dividend Tax Credit, meaning Non Registered accounts would be a good place to hold your Canadian Stock ETF, especially if you go that Big Juicy Canadian Dividend Route. And given that capital gains are taxed more favourably, the Non Registered environment is a good place for your stock, or stock-heavy funds.

Here’s a wonderful synopsis of what goes where thanks to First Asset, who by the way offer ETFs designed for tax efficiency.

Given that bond income and GICs and savings account income is taxed ‘in full’, you want to keep those amounts in RRSP/RRIF/LIF and TFSA accounts, as much as possible. And keep in mind that it is likely impossible to arrange all of your assets in the most tax efficient house as the need to strategically remove funds from RRSP vs TFSA vs Non Registered will come into play. We might need those bonds in the RRSP or TFSA to manage the risks. We don’t always let the tax considerations drive the bus.

Keeping it simple

Confused yet? Well ya, there are a lot of moving parts. Dan Bortolotti of PWL tells us that most self-directed investors will take a pass on the moves that are necessary to create the most tax efficient portfolio. Most of them will choose to stick with the wrap products for simplicity.

You might choose one of the Canadian asset allocation ETFs.

That said, if you are willing to put in the time and energy to learn the basics, you might be able to boost your returns (and income) by some .50%-1.0%.

And if it’s all too daunting, you may also consider to seek out help from a Canadian Robo Advisor such as Justwealth or WeatlhBar. ModernAdvisor also offers more robust advice, including a fee-for-service option. Justwealth offers the most extensive suite of ETF Portfolio models that includes Tax Efficient Portfolios. You can access a full holistic retirement plan, all covered in the regular fee schedule at Justwealth.

Who is Canada’s best performing Robo Advisor?

Keep Your Core Portfolio But Learn What Goes Where

Net, net, simple ETF portfolio asset allocation works. It’s the ‘what goes where and why’ that complicates the matter.

I’ll be back with retirement Part Deux 2, including some ETF portfolio options. We’ll also look at building that Dividend Growth and Income Model. There is a benefit that can be had by way of generous and growing income, to a point. I’ll admit to having a guilty pleasure of watching those big juicy dividends roll in.

Thanks for reading.

Please make sure that you know what you’re doing before you self-direct. If you don’t know what you’re doing, don’t do it.

Cut your fees, get some offers here …

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

You will also earn a break on fees by way of many of those partnership links.

Canada’s top-ranked discount brokerage

Cut the Crap Investing readers can earn a break on fees at Questrade by way of that partnership link.

Here’s Canada’s top-performing Robo Advisor.

I have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Consider Justwealth for RESP accounts. That is THE option in Canada with target date funds that adjust the risk level as the student approaches the College or University start date.

Our savings accounts

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are at 1.25%. You’ll find some higher rates on certain GICs. They now also offer U.S. dollar accounts. They have been awesome.

Our cashback credit card

We make between $60 to $70 every month! And that’s on everyday spending. There are no fees with …

The Tangerine Cash Back Credit Card

Kindly use the buttons below to share this post.

That was an excellent overview – thanks.

Thanks mkoskenoja,, not an ‘easy’ one to write I hope it does not read as too complicated. There are so many moving parts. Happy to answer any questions. If I don’t know the answer, I am happy to find someone in the know. Thanks for stopping by.

I think it got a little complicated by length but it was comprehensive so that’s what you get. I am an experienced dividend ETF investor/recent retiree so it was all good. For novices, the eye’s glaze over more quickly with this type of reading 🙂

Keep it up Dale!

Marko K.

dollar funds or stocks you might want to be careful as the IRA may come looking for you. Read

Great article One typo Believe you mean IRS. Not IRA

Ken k

Sent from my iPad

>

Thanks, yes that was a political typo. Thanks Ken.

my baseline scenario is that we [the u.s.] has a recession and then switches to an inflationary regime. as ray dalio has said, in a big debt crisis they always print in the end. in such a scenario bonds will not act as a “shock absorber” for stocks. thoughts?

Hi jk, nobody knows what will happen. That would be like going to a fortune tell. We need some mood lighting, candles and red drapes and such. If one believes in any doomsday scenario they might hold some gold as well? That’s part of the Permanent Portfolio approach. There’s a nice long term gold chat in this article.

https://inflationdata.com/Inflation/Inflation_Rate/Gold_Inflation.asp

Certainly anything can happen. But we can’t live and invest in fear. If we all go down, we all go down together. There are certainly times (1970’s) when nothing worked against inflation. But you at least still had some nice growth with stocks and bonds, just not enough to keep up with hyper inflation.

Thanks for stopping by.

Dale

You know Dale! Same thing i was finding.After read this blog, i will create easily the

retirement portfolio. Thanks

Thanks, feel free to send questions, or seek any additional input. Not a bad idea to check in with an advice only planner for this stage. I can suggest a few names. 🙂