Dividends are so popular. That’s an understatement. Government agencies have forced that upon us. We live in a low yield environment. Bonds come up way short in the task of delivering safer income for retirees. Naturally, investors turn to dividends. Can we live off of the dividend income?

The yield on iShares Core Universe Bond Fund XBB is about 2.8%. Not only that, the income has been decreasing.

Low income in concert with falling income is not sweet music to the ears of retirees. Bonds suck. That was the theme in should you roll the dice with your retirement savings?

In that article a financial planner argues that retirees should invest entirely in stocks. There’s greater growth potential in stocks. But with an all stock portfolio we have no protection from those nasty market corrections. The early 2000’s and the 2008 financial crisis chopped stock prices in half.

Living off of the dividends.

Dividend growth investors will offer that they can take the stock market risk out of the equation by ‘living off of the dividends’. A major risk for a retiree is called that sequence of returns risk. Selling off the stocks in a 50% off scenario in market corrections can kill the goose that laid those golden retirement eggs.

If a dividend investor generates the income that they need from the dividends there’s no need to sell the stocks in a market downturn.

Generous income and growing income.

The dividend growth investor turns the tables on that low income and falling income problem of the bonds. Stock dividends can deliver generous income and growing income. Typically you hear of dividend growth investors joyfully bragging about their 9% or 10% annual raises.

Did you get 10% annual raises when you worked?

Imagine that. You quit work but you still get a raise. Heck you get a raise that likely dwarfs the rate of salary increases you experienced when you had to battle through traffic to make it to the office. Look at Mike in that hammock. He’s lying around, collecting his ‘salary’ increases. He’s resting in that hammock but he’s living off of those dividends.

In the land of retirement funding chatter, we often talk about that 4% rule. The idea is that you might be able to start retirement by spending 4% of your portfolio value, and then allow for annual increases to account for inflation. It’s a useful benchmark but here’s why we also ignore that 4% rule.

Can you create 4% income today?

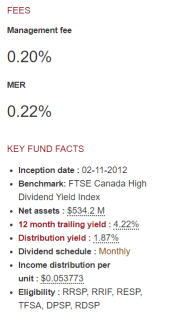

In Canada, that’s not problem. Even the Canadian high yield dividend funds are above that 4% dividend income level. For my wife’s accounts I use Vanguard’s Canadian High Yield Index Fund, ticker VDY.

We can see that the trailing yield is 4.2%. The dividend growth rate is choppy at times, but very impressive.

The first full year of operation in 2013 the fund delivered .75 cents per unit. That has increased to $1.33 per unit. That investor (aka my lovely wife) has enjoyed a raise of over 75%. Of course, that raise is just from the initial investment. I’ll write of that triple compounding that we can experience when we reinvest dividends and also add our new monies. Then, we’re really fattening up that goose.

That’s some goose. Some eggs.

The first reader who emails me with the historical figure who inspired ‘some goose, some eggs’ wins a Cut The Crap Investing coffee mug. OK, I don’t have any CTCI coffee mugs but if anyone knows the answer you’ve created a new task for me. I’ll get a hundred made and hand them out like candy.

Of course in the retirement stage when we’re simply living off of the dividends we have to rely on the fund increases in distributions or dividend growth from the stocks if we hold a portfolio of individual stocks.

Individual stock portfolios vs ETFs

For my personal RRSP account I have skimmed several holdings from the land of High Yield Canadian Dividend Payers. My income and income growth is a little better than VDY and my concentrated portfolio did not experience the dividend decline in 2016.

Here’s an income demonstration for every $10,000 invested, courtesy of portfoliovisualizer.com.

- Dale = Portfolio 1

- VDY = Portfolio 2

Certainly, I have concentration risks. I am counting on oligopolies over numbers of stocks. Don’t try this at home. Keep in mind that many advisors will also hate VDY as it is concentrated heavily in Canadian financials.

Big dividends in the U.S.A.

The comparable Vanguard fund for the US market is VYM. The yield on that fund is about 3.1%. That fund has been on a tear in regards to the price. The total returns have been generous and the dividends can’t keep up to the share price increases.

While the dividend growth over time is impressive, that fund delivered a sizable cut in distributions through the financial crisis of 2008. That’s not surprising. This is a US fund; the financial crisis was born in the USA. Many banks were generous dividend payers at the time and found their way into this index.

From 2008 it took 4 years for the income level to increase to new highs. Here’s the quarterly dividend graphic as per Seeking Alpha. Note: always double check your sources for any financial numbers, stocks and graphs.

The dividend investor might be prepared to live off of a little less. And certainly many do acknowledge the risks and accept the possibility that they may see some dividend disruption. They have replaced stock market price risk with dividend growth and health risk.

Our friend Mark Seed of myownadvisor is a dividend investor who is aware of the realities. He simply wants to put himself in a position where he does not need to sell any shares. He’ll accept some lesser income as well, if need be.

The dividend dream is alive and well.

Here’s Mark with why his goal to live off of dividends remains alive and well.

Here are some key thoughts from Mark.

- I continue to believe there are simply too many unknowns about the future. Having ample capital for our financial future will give us many options.

- If we are able to keep our capital intact we don’t need to worry as much about when to sell shares or ETF units when markets don’t cooperate.

- I don’t necessarily believe in the 4% rule – the ability to draw down your portfolio for 30 years (or so) without the worry of running out of money. It’s impossible to predict next year let alone 30 years.

- I find dividend income easy to track.

- It’s tangible money I can spend if and when I choose without worrying about stock market prices or gyrations.

- I agree with other investors – including many dividend investors – dividends seem to be more stable as part of total return than the hope of capital gains.

Caring for Clients

And here are some wonderful considerations from our friend Rona Birenbaum of Caring For Clients.

Interest in dividend equity investing has grown in popularity. There are a few driving forces behind the trend including:

- Low yields on conservative fixed income investments

- Lower taxation of eligible dividends vs. interest income

- Low cost of owning individual securities vs professionally managed equity portfolios

- Excellent performance of high quality dividend equities, ETFs, and funds and pools historically.

- Investor confidence in the strategy

A 100% dividend equity portfolio may not be optimal if:

- The dividend income is insufficient to meet cash flow needs and capital withdrawals are required. Selling equities during a bear market and subsequent recovery may undermine future growth of the portfolio and will reduce the dividend income the portfolio generates, resulting in an ever increasing need to draw on capital.

- If the investor is at risk of selling some or all of the portfolio during a bear market as a result of their stated volatility tolerance and/or their behavior in past bear markets.

- Many dividend portfolios we see are largely focused on Canadian investments. A properly diversified portfolio includes investments beyond our borders.

So will the dividends get the job done?

It’s a great strategy. Most importantly, it can help investors stay focused in the accumulation stage. It has the potential to help retirees stay the course during any market turbulence. That said it may not be all that easy to keep your eye on the dividends in a major market correction. Know thyself.

I am with Mike The Dividend Guy. While I enjoy my big juicy Canadian dividends, I feel that a dividend growth total return approach may be the most optimal. I have no problem harvesting Apple shares to take a trip or two. And quality rules. I did own VYM at one point. Research then led me to the lower income Dividend Achievers. That index fund and those companies help up much better than the S&P 500 in the Financial Crisis. The Dividend Aristocrats offered incredible stability in the last 2 major stock market corrections. I like the strategy of juicy Canadian dividends plus quality and total return potential for US holdings. I also feel it’s important to manage that sequence of returns risk.

Got dividends?

What about you? Do you have plans to live of of the dividend income? Or perhaps you’re a core couch potato investor even in retirement. That works too.

Please leave your thoughts in the comment section. Always invest within your risk tolerance level. Ensure you understand all tax implications. Consider some international equities as well. Seek qualified advice.

Dale

I think it was Churchill who said, “Some chicken, some neck!”. Not sure if he was referring to his dividends?!

Ha, thanks Jim. Yes you are correct. I believe I had a quicker response on LinkedIn, but I’ll get a few made up and get ya one. You only have to promise to post a pic of yourself using said Mug, at least once per week on at least 5 social media sites. If so, we’re good.

Thanks for playing, you’re a winner. Use contact form to get me your address for mailing.

Dale

Hi Dale – are we referring to Churchill’s “Some chicken! Some neck!? I am still in the accumulation phase so I’m not using dividends yet but certainly plan to when I get close to retirement. Very informative post – thank you!

Thanks Bob, hope you are well. Yes you are also a weiner, sorry winner. Very good. Another history buff. And I thought you just knew ‘everything baseball’. Send me your address for delivery. I’ll probably deliver it in person, drink one or your nice IPAs and I’ll be Even Steven.

Happy Friday, thanks for playing.

Dale

Good article Dale!

At 60 years old and retired I live off the dividend income of my ETF’s that generate $43K per year.

I sold off all my index funds 2 years ago and bought dividend funds after thinking about having to sell off investments to fund my retirement – as per your link to sequence of return risks.

While I resist the urge to tinker I am considering going 100% into dividend funds. I still have 20% of my investments in bond index funds (and another 20% in a preferred share ETF) but since I have enough income (my overall return in 2019 is 10.48% and dividend yield is 4.23%) I think I will wait for an equities correction, sell my bond funds and buy more dividend funds.

Thanks Marco. Keep in mind that traditional large cap funds will do the trick as well, if history repeats. In fact with some growth kickers and some risk management it’s possible that the core plus growth strategy could or would outperform the dividend growth approach.

They both work. It comes down to a personal preference. It comes back to what makes us comfortable and what can allow us to stay the course and sleep well at night.

If you know my writings, you know I am a fan of some risk management (bonds and other) for most any portfolio or approach. I am not a fan of rolling the dice …

https://cutthecrapinvesting.com/2019/11/20/should-you-roll-the-dice-with-your-retirement-savings/

Dale

That may be Dale but in my case I’m happy with the dividend payments and like Don I am not concerned with total return.

My wife is going to retire next summer at age 53 with a DB of $36K. Her dividend ETF payments will add another $12K per year to her income giving us a combined income of almost $100K a year – more than enough for us.

Good discussions on this subject matter 🙂 It’s amazing how committed people are to their thinking. I watched a Warren Buffet doc last week wherein the father of Bill Gates asked Warren and Bill what they attributed their success to – they both answered in unison – “focus”.

Being responsible for creating my own pension (was in a defined contribution plan), I am hoping to live off dividends and interest from my LIF and RIF accounts. The only CDN ETFs I own are bond funds. For CDN Equity, I have tried to mirror holdings of Dividend ETFs to avoid paying the MER. Fortunately, my portfolio is large enough to be able to hold a large number of companies and to diversify across sectors. For US, we do have some individual stocks (blue chips) and a sizeable amount of VIG. Thinking about adding some NOBL. Is it worthwhile to hold both NOBL and VIG or to simply add to VIG? Sitting on more cash than usual right now waiting for a correction and higher equity yields. Enjoy your posts.

Thanks Brian a fellow index skimmer, nice. I would see some benefit to adding NOBL as well. Past performance does not guarantee future returns but the Aristocrat performance in 2000 was incredible. 2 up years when the S&P 500 was crumbling year after year. Of course there were no dividend payers at all I’d doubt in the many profit-less companies that were driving the main index higher, never mind a 25 year history of paying dividends.

Combo might be more growth from VIG in the good times, more protection from NOBL when things crumble. Many financial planners told me they like a growth and defensive combination.

Dale

I’ve been living off of dividends for 15 years. It’s sweet! Don’t know how others of my generation are going to live if they think their pension is enough.

That’s positive confirmation Barry 🙂

Do you have all stocks/equity or do you also have fixed income?

I have some preferreds which I bought in 2009 when the world was coming to an end. My present portfolio composition – 20% preferreds, 70% Cdn and international stock holds (no ETFs) and the rest in cash in case I’m wrong about everything. They’re non resource large caps mostly with a long history of dividend increases. Pipelines, utilities, telecom and the banks. The more tax complicated stuff like Brookfield Infrastructure I keep in my TFSA. Canada Revenue filings in April are a breeze. This year my income growth was just under $4000.

Hey Barry, like the sound of that. I’m more of a fan of bonds for that insurance. But we all have our ways. Nice to read of your great approach.

Thanks, Dale

Thanks for the details Barry. It’s always good to read about someone who has been successful with their retirement finance planning. I hope you have another 15 years or more ahead of you.

Thanks for the details Barry. It’s always good to read about someone who has been successful with their retirement finance planning. I hope you have another 15 years of dividends or more ahead of you.

It works but you have to be very very patient. Starting young helps immensely. If not pray for a huge fall off the cliff “correction”. 2008/2009 was a gift as far as I was concerned … I rearranged my portfolio, sold the distracting stuff, and bought a LOT of quality stocks which fell “in sympathy” with the market … and here it is 11 years later and I’m glad I did. The best advice I can give is learning how to say a big “NO!” to a lot of investing information, even if it sounds ironclad and logical.

Remember Blackberry? Have a friend who bought a ton of it 10 years ago, swearing up and down with all the graphs and info at his fingertips. The only voice I heard in my head was “no growing dividend.” He’s still swearing today, if you know what I mean. Thing is he might have been right but I just kept hearing that voice.

Just buy the best of the best – TD, Fortis, Canadian Utilities, CN Rail, TC Energy, BCE for starters. Takes about 10 years of holding through thick and thin; all the stories you’re gonna hear. But after a decade you’ll be set with most of what you’ll own as it is unlikely ,with all the dividend growth while holding, you’ll ever get back to what you paid for it. I’ll leave the capital gains to my heirs.

Great post Barry.

Thanks Dale … I know our approach may be different but to each their own. Mine resonates well with my nature but I’m a lousy carpenter so I hire one to do the job.

Dale – thanks for the article. As usual, good stuff.

Barry – Excellent!! My wife and I are similar but we went the full 100% equities with only TSX dividend income/growth stocks and are a bit behind you in years of retirement.

Here’s our scoop for those that are interested. I’m 66.5 and have been retired for 6.5 years with no company pension. I took CPP right at 60 and OAS at 65. My wife is 62 and was stay at home so no CPP but she will take OAS right at 65. We only have 25 stocks and 2 ETFs (FIE,ZWB) in 5 sectors – banks, utilities, midstream, telecom, and REITs. No bonds, fixed income, or GICs but we do have a couple year cash wedge that we just keep in RBC Direct investing High Interest Savings (1.6% interest).

While working, I didn’t pay much attention to the investments and have never had an advisor. The two years before I retired (2011-2012), I went part time and got focused on the investments. It took a bit of reading and thinking but I decided on the dividend income/growth route and was glad I did.

As it worked out, we had incredible timing on picking up a good batch of dividend stocks at a discount in 2013 because of the big interest rate tantrum. We now have way more dividend income than we need to live off so have started gifted an early inheritance to our kids and their families.

We never trim or worry about asset allocation or diversification. With all the extra dividend income, I can never see having to sell something unless it’s a take-over or something goes really badly with a company.

All we do now is watch the markets as a hobby, play with the grandkids, spend time in the great outdoors, and sit back and collect our divys.

Ciao

Don

Hey Don, thanks for stopping by and for that wonderful comment. So nice to read that kind of success story. Yes when you’re covered by the dividends and you have a buffer, there may not be too much to worry about. I would still protect to a modest degree, I’m consistent on that theme ha.

If you travel to US or other, you might consider from US and International equities without a currency hedge. Canadians have lost big time against the US dollar of course.

All the best, and congrats.

Dale

Yes Barry, I remember the heady days of RIM as I had one of the original BB devices while I was working at AT&T’s global account group in Toronto.

A colleague of mine, with an economics degree, had his entire RRSP in Nortel in 2000 and was buying more at $115/ share. Poor guy lost it all.

I like dividend ETF’S and keep my average MER under .4%. I know I could eliminate that completely by buying the stocks but I like the diversity the funds provide.

Great article. I believe you have to look at where your retirement income comes from. I have a DB pension and when combined with CPP and OAS will give me 75% fixed income exposure. The other 25% is invested in solid dividend paying Canadian stocks and ETF’s. International exposure comes from Pension (40%) and CPP (85%). All Canadian so I don’t worry about exchange rates or foreign taxes. Love seeing those dividends pour into account each month. Without the pension I would still take a high equity risk.

Hey great comment Gruff. We might take into consideration the asset allocation of our pensions. But I’m not sure. Do we get any added benefit if the US and International does well, other than the pension being funded. They’re not going to give us a raise?

All said, if one travels to the US a bunch, they can benefit further by holding some US assets in US dollars to eliminate the currency risk for travel. Ditto for international travel.

You mix looks awesome, 75% in pension ‘stuff’.

I am a fan though of protecting and maximizing each bucket : )

Dale

Nope, I don’t buy it. I understand the behavioural appeal of focusing on dividends, but a dividend focused portfolio gives you a concentrated portfolio (you are excluding non dividend payers) which will therefore give you a wider dispersion of returns (less statistically reliable) which on average will be less than a more diversified portfolio, due to the skewness of stock returns. Dividend focused portfolios are also less tax efficient.

I prefer a total return approach which, being more diversified, gives you the best shot at the optional outcome. There are also better ways to deal with sequence of return risk – an allocation to bonds/cash etc.

https://www.etf.com/sections/index-investor-corner/swedroe-irrelevance-dividends?nopaging=1

Thanks Grant, can’t say I disagree with you as they can both work. And we do have to be careful of that concentration risk. That said, the Canadian market holds sectors that I don’t want to own. I like the total return approach, but I think we can shade the portfolio, especially for retirement.

And yes we should keep in mind that nothing is more important than investor behaviour. The divs do wonders for many.

Thanks for stopping by.

Dale

Yes, I agree, to shade the portfolio, especially in retirement is not terrible. I just don’t like to see people dump their indexed portfolios at retirement to invest in dividend payers thinks they should live off dividends. And, yes, there’s nothing more important than behaviour.

Hey Grant

Each to his own for sure depending upon their situation and goals. My wife and I don’t really care about total return. All we care about is dividend income to live off and we have more than enough of that. Because we buy and hold, any extra capital gains at this stage are just going to go to a combination of our estate and taxes.

Also, all the tax calculations I’ve ever done show that dividend income is taxed at quite a bit lower rate than both income and capital gains. I’m in Alberta and any Cdn eligible dividend income in the $47-95k net income tax bracket gets taxed at a marginal rate of 7.5% compared to 30.5% for income and 15.25% for capital gains.

What exactly are you referring to when you say: “Dividend focused portfolios are also less tax efficient”??

Ciao

Don

Don, I think total return is important as that is the source of cash flow in retirement. Both yield and capital gain creates your cash flow. I don’t want to ignore the capital gain component because then I have to save more for retirement and then will be left with a pile of unspent cash when I die.

It’s true that dividends are more tax efficient than capital gain up to about $80k, but I’m thinking more of the accumulation phase. You are reinvesting dividends so it is a big tax drag having to pay tax, then just put the remainder of the money straight back. Better not to get any dividends in those years. In retirement, too, the dividend gross up can put in you in OAS clawback territory.

https://www.moneysense.ca/save/retirement/a-better-way-to-generate-retirement-income/

Hey Grant

We invested differently in the accumulation phase than our retirement phase. (see my earlier post from Nov 23 at 1:39 for our details and how we have WAY more dividend income than we need to live off so never have to touch our capital). That means total return doesn’t affect our cash flow in the least. It only affects how big our inheritance will be, My wife and I are also more than fine leaving “a pile of unspent cash” to our kids and families. They’ve been great kids and grandkids and have given us huge enjoyment .

I have also done a thorough tax analysis including OAS clawback as well as total lifetime taxes. I love that taxtips,ca website and Excel to summarize.

When the dust settles, I just don’t like it when people try and say this is the best way to invest as it really is each to his own and what works for one person may not work for another. I’ve put a fair amount of effort into our investing strategy and am totally pleased with it and know that it works for us.

Ciao

Don

Don, I totally agree with you that there’s no one best way to invest that works for everyone. Behavioural factors, being able to sleep an night etc. is the most important thing. So long as the investment strategy is sensible, it’ll work out. It sounds as thought you have done great , have more than you need and want to leave some for the next generation, so many strategies in that setting will work just fine.

I think it’s interesting, and useful, though, to learn about different strategies. I find, too often, that people will only read about their own approach (confirmation bias) and are too ready dismiss anything that creates dissonance with their own view.

All the best,

Grant.

Hey Grant

Thanks on this last note. That’s good to see on the “no one best way” and “sleep at night” comments. On this, we both totally agree.

That’s also an interesting comment on “confirmation bias”. I do read quite a bit on different approaches but only out of interest at this stage. I will definitely admit to being set in our ways in terms of investing. I’ve found something that works for us and do not want to try and optimize it any further as there would be some risk in doing that. I might be leaving some money on the table but I don’t care as long my wife and I have enough to live off no matter how long we live. (and the inheritance is just an extra bonus)

I actually just read the article from the link and think it is total BS. I really find it hard to believe how many so called financial experts say that taking a cash dividend and selling a few shares are exactly the same. The net cash result might be the same but selling a few shares means that your total future dividend income is now reduced.

An even bigger factor is that it means that the investor has to decide how much of which stock to sell. In my opinion, that is a very stressful situation especially compared to just holding what you have and collecting a solid ongoing dividend.

As I said, each to his own. I just don’t like these arrogant financial people hammering dividend income/growth investors. Saying something like a dividend income investor invests that way because they can’t control their spending is absolutely ludicrous.

Yes to each his or her own. I just googled ‘dividend investors are not stupid’ and look what came up …

https://seekingalpha.com/article/4265199-sorry-dividend-investors-stupid

One of my articles on Seeking Alpha. Ha. This is a situation where we can all be right. As long as we understand the risks and know what we’re doing.

Dale

Hey Dale

Beauty!! I had previously read that one and it, along with some of your comments on My Own Advisor and some of your other articles got me started following your work through Cut the Crap and Seeking Alpha.

I really enjoy how you present stuff and how you are always very careful to stress that there are many ways to invest and each to his own.

Thanks mucho for your articles and keep up the most excellent work!!

Thanks DAG, I appreciate the kind comment. I do like the Seeking Alpha mantra.

Read. Decide. Invest.

Dale

Don, it is the same thing. If a share pays $1 in dividends, the value if the share must go down $1. Dividends are not magic. You then either have the same number of shares that are now worth less (the shares that pay a dividend), or less shares that are worth more (the non dividend payers that you sell a few shares to create your home made dividend). Both the capital component and dividend then continue to grow.

I agree that Larry Swedroe can be provocative in his writing style. But he is a very smart guy, widely published, and the Director of Research at a large wealth management company. Everything he writes is backed by peer reviewed academic research. I wouldn’t be too quick to dismiss what he says.

Hey Grant

As I said, I realize the net cash is the same but if you have less shares of a dividend paying stock, then your dividend income will be less. After this many years of investing, I obviously know how dividends work.

BUT, in the end, it is not the same thing as you will have to decide what stocks to sell and this is not an easy thing to do especially compared to just sitting back and getting all your cash flow from dividends.

Hey, I know it works as I’ve been retired for 6.5 years and have given our kids $200k of early inheritance so far and much more planned. 🙂

The ongoing debate between “total return” and dividend investing is interesting but I do think that what’s “best” is just a story of finding value in your life. Some people are thrilled buying property and renovating only to sell at a later date for a capital gain. Others like myself would enjoy finding that one well built/maintained building with stable tenants who are thrilled to reward your ownership with higher rent every year. The latter is announced by SMS while you’re in the Alps enjoying an exceptional home made Schnapps at a family run kneipen during a glorious mid afternoon hike.

Happy with our dividend investing approach. The single largest holding is VYM, followed by the iShares XEI. There is also a smattering of smaller dividend tilted holdings, such as SPHD, ZDI, VYMI, ZWE, ZWH. We only need a 4.25% return before inflation to meet our goals. If we can get that almost strictly from dividends, the psychological aspect is covered. Works for us although we understand there is some tax inefficiency in our large non registered account. That said, about 30% of the portfolio is in XAW for a more total return approach. We plan on holding on to that one and VYM forever. Total yield is 4.23%, right on target.

Thanks Rakiki for sharing your approach and an overview of your holdings. It’s awesome that readers will share and let others look under the hood. That looks like a great mix. Canada / US / International including developing markets. You have some total return slant in there as well. And that generous income that you’re looking for.

Nice to read that you’re likely in a very good place with your portfolio assets given that you have a sizable non registered account.

I am a broken record, but I would still protect that income with some lowly bonds, ha. Even just a very modest amount to help in any severe market correction and potential dividend cuts and holds. IMHO we can use bonds to cover dividend income as well as helping with that sequence of returns risk. That said, you may accept the risks and are prepared to spend less if need be.

Thanks again, I hope you’ll continue to stop by and share your progress.

Dale

I agree with having some bonds to smooth the ride. For those who can’t stand the idea of having anything other than a 100% equity portfolio I like Nick Murray’s advice of keeping 2-3 years of cash aside in separate account. When the equity portfolio is down 20%, stop withdrawing from it, (reinvest dividends) and switch to the cash account. Spend from the cash account until the equity portfolio has recovered to about the 20% down point, then when fully recovered, replenish the cash account. Not fool proof, but safer than 100% equity only. Nick Murray’s book “Simple Wealth, Inevitable Wealth” is fantastic.

Bingo about the cash cushion. We plan on starting retirement in about 5 years. A nice HISA/GIC to start complemented by the income from our holdings will tide us over. We do have about $150K with WealthBar in one of their low volatility private portfolios and will draw from that in the first few years. (Fee is too high, but it’s a bit of protection and has been steady at 7-8% for years with a 4% yield.) No need to touch anything else in case of a 3-4 year downturn. And yes… two DB pensions to pad the wallet. That said, the dividend portolio is a bit overcomplicated. We have 11 individual holdings as well (all time favourites BEP and BIP, BPY, RY, BNS, AQN, FTS, BCE, CM, ENB, NPI). Your site is excellent and as a personal finance nerd, I enjoy reading through!

Hey Rakiki, great to hear about that private pool portfolio addition at WealthBar. I am researching and working on a post on that offering. I think that is a great addition. I think it’s worth the costs. That’s a wonderful add on and I’ve suggest to a few readers that they have a look.

One question though, would it not be more advantageous to draw from any higher risk assets early in retirement if we’re lucky enough to have them perform very well? And we’d save the cash as well for when it’s needed? Of course we have to keep a healthy enough allocation to stocks for growth throughout the process. Wondering if you’ve thought about that, or conducted any research on the matter.

As you may know the Wade Pfau’s of the world are not fans of cash bucketing 🙂

Dale

Thanks Grant. I am more of a fan of bonds, but maybe a mix of bonds and cash is ideal. I think you can use less bonds compared to cash as they offer that inverse relationship, when REALLY needed. Yes there’s no guarantee but bonds have done their thing in every recession – US studies I’ve seen.

I will write a post on the subject of bucketing, I’m in the writing/research stage, but I think the best use of any bucket is to supplement the stock harvesting, so we can sell less stock. Of course when things get really bad we might have to cut back on spending levels – that dynamic spend rate.

Interesting topic for sure, bonds vs cash buckets, and combinations of.

Dale

Hi Dale, excellent point. I have modeled our income needs. In summary, we have a 14 year gap between quitting work and starting our DB pensions. Hence the income oriented portfolio. So let’s say I have calculated 100k cash/14 years. 150k WealthBar/14 years with inflation adjustments. Plus (considerable) other income from the rest of the portfolio. That works just fine. In a colossal crash we would hunker down and dip into cash or even our margin account excess or HELOC. Instead of crystallizing major losses, we would borrow a bit at 4% ish and wait for a recovery. All fun stuff!

Hi Rakiki so nice to see you cover the bases and put in the time to understand the risks and make the appropriate moves. Yes, the HELOC is overlooked as a retirement funding source on an ongoing basis (in moderation) and during a market correction.

One can use a HELOC partially as an emergency fund and as a stock market emergency fund.

Thanks again for adding so much to the site.

Dale