I have penned often on the wonderful Questrade ads that suggest that you can retire with considerably more wealth. The key or suggestion is that you ditch your expensive advisor and their expensive mutual funds. You can retire with 30% more wealth. I also often suggest that is just a starting point. With a sensible low fee investment plan you might retire with two or three times as much in the bank.

I really like this article from Robb Engen, it was also reposed on findependencehub …

Yes, you can retire up to 30% wealthier.

In that post Robb looks at the real numbers comparing some widely held Canadian mutual funds to a low fee index based approach.

An advisor fights back.

It is a response to the challenge of financial advisor Jason Periera who had counter punched with …

Here’s the link to Jason’s post.

I have had my friendly debate with this topic with Jason on Twitter. You can follow me here @67Dodge. Jason’s problem with the Questrade television commercials is rooted in what they leave out – the value of advice. But that might be a moot point. Investors at Questrade who invest in the Questwealth Portfolios have access to advice, including financial planners. The portfolios are also managed.

That said on many counts Jason offers a fair article with some honest and relevant perspectives. He is not ‘anti-Robo Advisor’. Quite the contrary …

Third, I have – on countless occasions – praised robos for making investing more accessible and easy for investors who only have small amounts to invest. Let’s face it, it’s pretty remarkable that you can open an account, be directed to a modern-portfolio-theory-designed portfolio matched to your risk tolerance, and rebalanced as needed, starting with just a single dollar.

– Jason Periera

And I don’t think Jason is one of the threatened advisors I was alluding to when I posted real advisors will not be intimidated by those wonderful Questrade commercials. Jason is merely responding to the fact that there is incredible value in advice. That is undeniable. But the reality in Canada is that Canadians largely get no advice or poor advice to go along with very poor performing mutual funds.

That’s not an opinion. Canadians have showed me their results and have detailed how they are treated. In my opinion the Questrade commercials are valid, and needed in Canada. They perform a wonderful public service. Of course, a 30 second commercial can’t even begin to paint the full picture.

I’m with Jason, in that the Canadian Robo Advisors are a wonderful option. In my opinion, that is the place for most Canadians currently stuck in poor performing mutual funds.

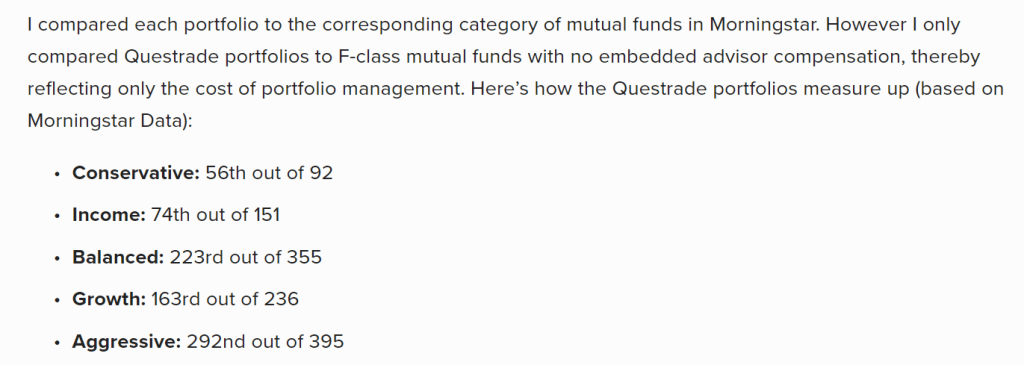

Be careful with your benchmarks.

In Jason’s post he compares the Questwealth Portfolios with F-series mutual funds. The f-series funds will not include the trailing commissions that go to the dealer (advisor). And certainly the performance is mediocre …

But again, the Questrade Portfolios (and all Robo offerings) include advice. Apples to apples would mean we would need to include the cost of advice. Remember an advisor might be paid from the mutual fund fees. One can also access a fee for service planner. There are many models for how your advisor or planner can get paid.

Back to Robb’s comparison.

Robb’s analysis focuses on the comparison of big bank mutual funds and the in-house index funds such as the TD e-series. And it’s certainly no contest. Robb demonstrates how one would build greater wealth by way of the lower fee index options.

In fact Robb even looked at RBC’s biggest fund (and Canada’s biggest) – the RBC Balanced Fund. Of course I had penned that Canada’s largest mutual fund is not so bad. That’s true. But you can do better as Robb demonstrates.

This week I updated that post to include the performance through the recent correction. Once again – not too bad.

And beyond the index funds, an investor might better off in a one ticket asset allocation portfolio. Those are managed for you, but you would have to open that fund by way of a discount brokerage. They are for the self-directed investor.

More Weekend Reads.

Mark offers his July dividend update at myownadvisor. Mark (and his wife) is now 68% toward the end goal of the semi-retirement life.

Can’t wait to welcome you into the club Mark.

And on MoneySense I make sense of the markets for the week. Once again, it was an eventful week and post.

Also on MoneySense Jason Heath offers the best way to help kids financially.

And in addition to my MoneySense weekly I am more than excited to be part of the Million Dollar Journey writing team. That is one of the most-read blogs in Canada and I’ve been a fan for many many years.

Here’s Calculating your Adjusted Cost Base – ACB.

GenYMoney also offers a July dividend update.

And continuing with the July dividend parade here’s Passive Canadian Income.

And Mathew reports a record month on All About The Dividends.

On the economic front.

Here’s John Mauldin with the prospect of European resurgence. We’ve also seen Canada with some economic numbers such as employment that are better than US performance.

Here’s a subject that I’ve been researching. Happy to find this on findenpendencehub – The illusion of holding gold through some ETFs and funds. I hold a couple of ‘gold-backed’ ETFs.

And I know that most readers are not Globe subscribers, but here’s a wonderful article on how the pandemic has changed Canadians’ spending patterns.

Certain sectors are greatly impaired. And the situation is not likely to change in a hurry. The new normal is here to stay ‘for a while’.

And of course we’ve moved online to shop and that will affect REITs.

Scott Barlow had mentioned that BMOs’ Brian Belski had suggested that REITs were a better place for yield-hungry investors compared to utilities. That said, the analysis looks at some historical trends, not the situation in the new normal. Again see that retail analysis link and connect the dots.

I’ll try to connect the REIT and consumer dots that also includes the work-from-home economy. Stay tuned.

We’ll see you in the comment section. Will you retire with 30% more wealth?

Canada’s top-ranked discount brokerage.

Cut The Crap Investing readers can sign up with Questrade (Canada’s top-ranked discount brokerage) through this partnership link. You can buy ETFs for free, including the wonderful one ticket options.

While I do not accept monies for feature blogs please click here on the mission and ‘how I might get paid’ disclosures.

Kindly share this post with the buttons shown below.

Dale

Thanks for the mention!

Yes, I’ve been seeing your name everywhere! Congrats on the extra freelancing pieces. Have a great weekend.

My pleasure. Thanks for stopping by.

That chart on how Canadian’s expect their spending will change is really interesting to consider in the context of which sectors will do well or lag going forward. Cutting entertainment and restaurants is not surprising, but on the other hand I would think people would be spending more on groceries now than the chart expectations.

Folks have changed of where they spend their monies, how they spend, and certainly how much. We are saving more as well and paying down debt. Interesting trends to follow.

Excellent! Especially Robb’s article, confirming what I had already learned TD’s E-series funds.

Yes that was a great comparison.

Nice read. I follow you on seekingalpha and recently ran into this site. I am more in the camp of individual stock holdings and dividend growth investing. REITS have definitely been hammered. RioCan is down and hasn’t recovered since March.

I commented on RioCan and posted a link to a great video in my most recent post. I’ll keep watching the REITs.

Dale