Unfortunately I am not talking about my own Apple stock holding. I’ve done very well with Apple, initiating a position in 2014, and adding a few times soon after. I then trimmed a few times creating homemade Apple dividends to help fund trips to PEI, starting in 2018. But my Apple holding pales in comparison to a reader who received a financial review in the Financial Post. He had way too much success with Apple stock, if that’s possible.

Of course the ‘too much success’ is a wonderful problem to have. In that Financial Post article we read that the bulk of the investor’s wealth is in that Apple stock.

Their cost was about $41,300 based on the exchange rates at the time. Today, that Apple position is worth $3,360,000 and makes up a significant chunk of their net worth of $4.4 million

Once again, that is a great problem to have. And obviously there is too much concentration risk in one company. Even if one sees that as a wonderful company with very strong long term prospects. Of course, I am biased, I see Apple as a wider moat ‘lower risk’ stock over the longer term. Apple has an incredibly strong brand and a very loyal customer base. They are diversifying away from a reliance on iPhone sales and are creating repeatable income by way of subscriptions and paid services.

What happened to disruption?

And they sit on a mountain of cash. All said, it’s only one company that operates in a sub sector with the potential of incredible disruption. Personally, I find that in recent years there has been a lack of ground-breaking disruption in the smartphone space. Companies such as Apple and their competitors are only making incremental improvements in camera or enhanced features or power. That lack of true disruption is a plus for an Apple shareholder. There’s been no biggie to knock King Apple off of its throne.

My love for Apple stock and products aside, there is stock market risk, individual stock risk, economic risk, pandemic risk, inflation risk etc. Those risks need to be managed and some Apple stock needs to be sold. The question is – how much Apple stock should be sold?

Sell all Apple and create a $1.4 million tax bill?

That appears to be the suggestion from the financial planner who is offering advice in the article. You’ll read in that article that the husband and wife (Bill and Cindy) want to buy a new home and need to raise monies for that purchase. But sell all of that stock and send the taxes to Ottawa?

Why the rush to create that immediate cash? Borrowing costs are at record lows. Bill and Cindy could get a mortgage, perhaps even at 1%. There is no absolute need to pay for that house in cash. It is a great time to be a borrower.

Sell enough Apple to protect against a market downturn.

I’m not a financial planner, but here’s my back of the napkin thinking. $390,000 of the Apple stock is in TFSA tax free savings accounts. I see those TFSA accounts as an option to sell some stock and add some diversification. Perhaps they sell $140,000 of Apple stock leaving a healthy $250,000 Apple holding. Of course it’s a tax free account, there will be no tax consequences.

That investor then might use that $140,000 to buy US and International stock ETFs, plus bonds that might include Canadian, US and International bonds. I had penned on the Vanguard Global one ticket bond ETF. I would also add some gold ‘stuff’ and bitcoin.

Canadians can hold the 3iQ bitcoin fund in a TFSA. Full disclosure, I hold that fund.

Prune that Apple tree over several years.

With respect to the non registered Apple stock holding, I would consider selling that down over several years. There’s almost $3,000,000 of Apple stock. If that investor has that longer term faith in Apple they might sell off $400,000 per year over several years and move those monies to a conservative blend of stocks and bonds. They might even consider Horizons one ticket ETFs. They are corporate class and tax efficient. Once again, I would top them up with some gold and bitcoin and cash.

Given that the investor from the article had $65,000 in unused RRSP room, the tax hit from the stock sale in year one might be in the neighborhood of $90,000, as an estimate.

The investor could then create retirement income from the TFSA account, from a portion of the Apple non registered share sale proceeds, and ongoing, from the new balanced mix in the non registered account. They have RRSP funds to draw from as well.

It’s a balance between the tax hit and the risks of stock markets and the concentration in Apple. Spreading out the Apple stock greatly reduces the tax hit, but it increases that stock market risk. That said, with a more balanced portfolio even in year one, there may be no need to sell Apple stock if it falls precipitously. The investor can wait it out, and take monies from balanced holdings in the TFSA, RRSP and non registered accounts.

What do real planners think?

Once again, I’m not a planner. That is my quick reaction to the horror of a seven figure tax bill. I will contact a few financial planners to see what they have to say. I’ll follow that up with a new post on this Apple problem. If you’re an advisor or planner and you’re reading this and want to give it a go, send me a note via that contact form.

Here was one option offered …

Would create a synthetic sale with a bank. Delay capital gains for 5 years. Get 90% of the value of stock to diversify. Easy peasy.

Stay tuned.

The Weekend Reads.

On Savvy New Canadians, Enoch has a very nice overview of investing in ETFs.

And on that subject I was more than happy to offer this co-production with our friends at Horizons – How to build the Balanced Portfolio with ETFs.

This week on MoneySense I took a look at Canadian pipelines and also a very interesting message from Elon Musk to his employees. We take a look at how the Canadian stock market is fighting back.

And here’s the weekly newsletter from The Sunday Investor. Click on Week 50. There’s an incredible compilation of graphs and charts, including …

You’ll also find the weekly breakdown of asset class returns, and returns of each stock within each sector for the Canadian market.

On findependencehub Jonathan Chevreau asks if it’s a good time for a travel and leisure ETF. A common theme that I buy into is that the pent up demand for travel and experience is incredible. That will be unleased when we get to the other side of the pandemic.

This week on My Own Advisor planner Steve Bridge stopped in to detail what a financial plan should cover.

Banker on Wheels offers a wonderful look at his around-the-world biking adventures, and draws parallels to the investing experience.

Here’s how to invest like the Ontario Teacher’s Pension Plan.

Stocktrades.ca goes against the grain and takes stock of bonds.

On Million Dollar Journey Expat Kyle Prevost takes a look at the best ETFs for Canadian Expats.

And here’s a look at the November dividend update on GenYMoney.

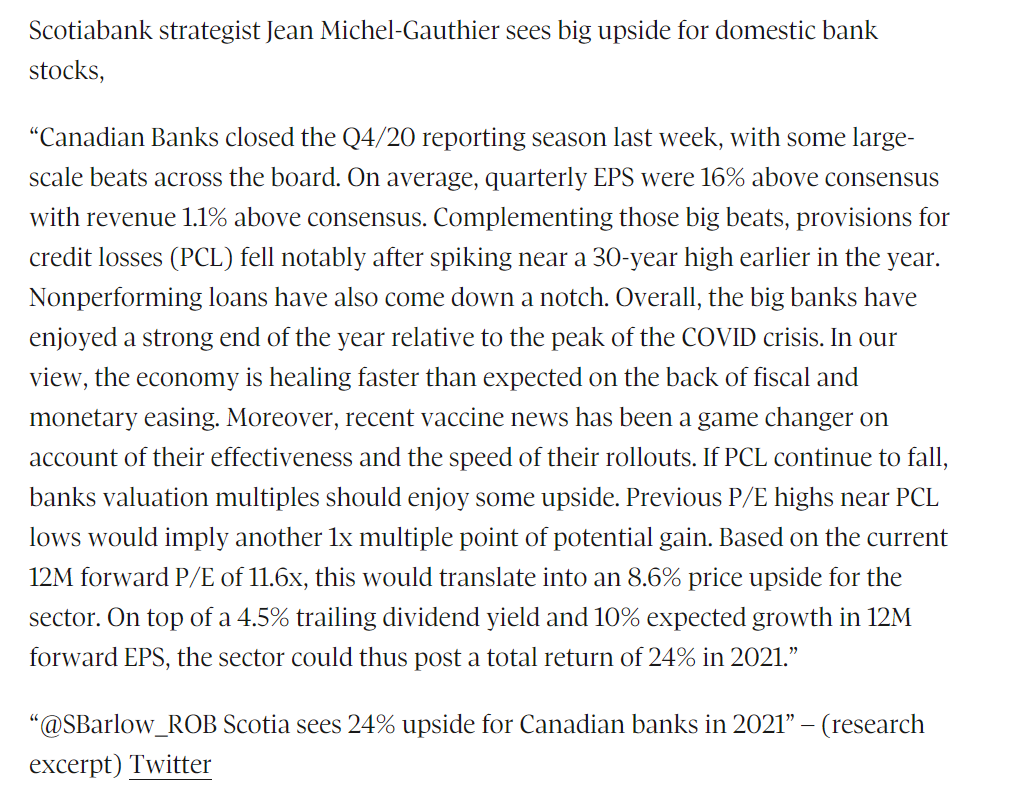

Canadian banks stocks. 24% upside?

A Tweet from Scott Barlow. I’ll take that 24%, thank you very much.

Thanks for reading. We’ll see you in the comment section. What would you do if you had more than $3,000,000 in one home run stock?

Partnership links.

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads, and hence, easy to read.

Check out EQ Bank for those who want to make their cash work a lot harder. The current high interest savings account rate is 1.5%. EQ Bank recently introduced RRSP and TFSA accounts with a rate of 2.3%. You’ll also find GICs.

I also have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple and Questwealth from Questrade.

Dale

Not a planner here but my answer to your question : donate some stocks to a registered charity such as Salvation Army or whatever cause is close to your heart. No taxes payable on huge capital gains on donated portion, and charitable tax receipts will offset capital gains on other portion. The feeling of supporting a worthy cause and helping others who are in need: priceless!

Thanks Linda, yes I think many planners will come back with that generous charitable giving as part of the mix. And it’s such a great opportunity to give as well after such incredible gains.

Thanks so much for stopping by.

Dale

Well if they’re going to sell any from their non registered account I would do it before the end of the year. I think that capital gain taxes are going up to 75% to help pay for the mess we’re in. That’s what I’m doing with my perpetual preferreds I bought in 2009. In 2 years if I’m still around I’m collecting OAS at age 70 … $10,000 approx. If I collected now about half would be clawed back. The preferreds mentioned are over $25 and one from Power Financial will be called at the discretion of Power Corp – they announced “at some point” when they decided to dispense with the common shares (PWF) on the tsx. Also the sale will be offset by losses in Shell and Interpipeline. I’m trying to think ahead of the curve!

I can use the cash for fun and games before decrepit health sets in … something I’m doing my very best to avoid by rigorous walking/biking/hiking and home prepared quality meals. In the latter having a Hungarian wife helps. So far so good.

Thanks Barry, difficult to plan based on what the government might do, but I hear ya. I think they will have to find ways to pay our way out of this at some point. Cap gains is a likely target, but when?

Are you still in a lot of pref’s?

Dale

When I sell PWF .H (presently $25.43) and GWO (presently $25.24) perpetuals I’ll be left with BAM.N ($23.74) and CIU.A ($23.91) perpetuals at about 10% of my portfolio. In 2009 I was 30% in perpetuals – CIBC called one and the others I sold. The remaining two can do what they want … as long as the income keeps coming. Selling off the first two with very little future price appreciation prospects will bring down the income for next year but a six digit wad of cash from the sale will offset that. We always have surplus cash at the end of the year which we plunk into our TFSAs . It’s a modest lifestyle. The sale minimizes clawback of the 10 grand in Feb 2023. By the way – make sure you apply for OAS 11 months before your 65th birthday because it takes a long time to process the application, unless you’re automatically enrolled.

I would absolutely start selling some. Slowly.

Some things just don’t add up though in the article.

I mean, he makes $4,200 per month.

She makes $0 as a homemaker and yet they have > $3 M in Apple stock, and want to buy a home in Vancouver after upgrading the condo and retire in 5 years??

Geez….

Sell some units slowly over 2021. Use proceeds to invest in more diverse basket of income-producing assets and index-based products. Max out TFSAs, RRSPs, RESPs for child and also buy the home if they wish. That still leaves ~ $1.5-2 M to be invested and could likely earn easily $50K per year, cash for life.

“Bill and Cindy would like to have $100,000 in retirement income after tax and to retire in five years.”

That money will double in another 10-12 years if left untouched.

They can retire now if they cut some spending or he could work part-time to keep him busy. All good there. We all need purpose in life.

There is no way if I had >$3 M stock portfolio would I be a) having that in one stock and b) would I be working full-time. Just me!

Find myself in a same predicament. I am an Apple employee, worked there for 15 years, and still going, have been enrolled into Apple’s ESPP since 2007, taking 10% off pay check, but did so for many years while still a student working part-time, then taking care of a sick parent. Currently find myself with an Apple Stock portfolio approximately $475K CAD.

By far my biggest position in my portfolio, but also have a maxed out TFSA with index ETFs, work RRSP almost maxed out containing index ETFs as well individual individual dividend earning stocks and a non-registered account dabbling with individual dividend paying stocks.

I’ve never sold one share of Apple stock since 2007. I’ve probably spent about $30K USD from my salary, and of course it has paid off as I’ve had an incredible return, but I’ve often wondered when I should scale back and sell some off.

Personally, I plan to hold them for at least another 5-10 years or more, but I also wonder about the impending doom of our post-pandemic economy and if rules will change with a 75% capital gain tax which would obviously impact my return, so I’m left with wondering, what should I do? Sell little now? more later? or sell most now and leave some for later?

Don’t get me wrong, good problem to have, but does leave me a little uneasy considering it’s my biggest position by a lot.

As an ex Apple employee (11yrs) I completely understand the situation that you’re in. What you must do moving forward is cash in the new stocks as they are rewarded to you. The capital gains taxes are paid by Apple at that time and and reset to zero. So any gains made from that moment moving forward can be taxed. So you have two options. 1) reinvest the funds, buy Apple stocks if you wish or diversify, that you just cashed out inside of the TFSA as your contribution for that year. Any growth is now Canadian tax free(-withholding tax from the US. Which is paid in either vehicle so it’s a wash.)

2) invest in a whole/universal life insurance plan with those funds. As those funds grow you can take out a secured loan with any bank for the cash value of you investment. In stead of selling off portions of the investment. As long as the interest is less than the growth. It will continue to grow. Upon your expiration date the bank will receive the funds necessary to pay off said loan. This allows your investments to grow and never be cashed out paying a capital gain tax. Whatever funds remain also pass on to the beneficiaries tax free as that’s how insurance works.

Of course there are many other factors involved in this type of situation. One of which is qualifying for the insurance.

In the very least option 1) is a must do.

Over time roll over your remaining Apple stocks. There is no way to avoid paying capital gains taxes on those. However if rolled over on a yearly basis it will spread out the taxes over time instead of one large lump sum.

Thanks Mano, yes that is a good option for those who have the ability to go that route. All said, it’s an option that one should explore if they are in this situation.

Thanks for stopping by.

Dale

I thought I was overweight AAPL but his takes the cake! But I’m with you: They could easily borrow money for the house and them pay it off over time with sales of chunks of shares. They could sell $538 now tax free: all of the TFSA $390k plus $148k non-reg (2x$74 RRSP room). Then sell chunks over time -enough to at least get them up the threshold of the top tax bracket for BC (Federal its $216k, each? not clear who owns the shares) until they get down to a better %age-maybe Buffett’s 25%? . I would put the money into Canadian blue chip dividend payers like banks, telecoms, utilities and some SPY. But a high quality problem.

I also agree with this comment. If they want to buy the house sell everything that is available tax free. Borrowing cost are very low and will remain so for a long time. Then every year sell an amount that keeps them in a managable tax bracket. (will have to pay taxes at some point). Take a long term mortgage and use the proceeds from future sales of shares to pay it down. Then also each year put as much as possible back into the TFSA’s since your allowed to replenish them the year after withdrawal. I would also borrow any lump sum payments to the mortgage back to buy quality dividend paying stocks. The interest on the loan would be less than the dividends, and they would be tax deductable. I wouldn’t sell out fear of the tax rate changing. Who knows if or when this might happen.