One of the biggest risks to stocks is bonds. The great fear is inflation and a rising rate environment that might come along for the ride. But as I discussed in my most recent MoneySense post, a rising rate environment might not necessarily accompany inflation. After WWII, we had some meaningful inflation and rates stayed low. And speaking of meaningful inflation, this week delivered a mild inflation shock as the U.S. CPI reading was well above estimates. On the inflation watch for investors, most are wondering if inflation will be lasting, or is inflation ‘transitory’ – just passing through?

According to a recent CNBC post, inflation in April accelerated at its fastest pace in more than 12 years as the U.S. economic recovery kicked into gear and energy prices jumped higher.

The Consumer Price Index, which measures a basket of goods as well as energy and housing costs, rose 4.2% from a year earlier. A Dow Jones survey had expected a 3.6% increase. The month-to-month gain was 0.8%, against the expected 0.2%.

That inflation spiked spooked stock markets for a few days. From Trading Economics …

It is the highest reading since September of 2008, amid a surge in demand as the economy reopens, soaring commodity prices, supply constraints. There is also a base effect weighing as the coronavirus pandemic dented economic activity bringing the inflation rate to 0.3% in April 2020. The biggest increases were recorded for gasoline (49.6% vs 22.5% in March), fuel oil (37.3% vs 20.2%) and used cars and trucks (21% vs 9.4%).

Rising rates are not a given.

Here’s the link to my most recent Making Sense of the Markets post. And here’s the surprising chart on inflation and rates, courtesy of Mike Philbrick of ReSolve Asset Management.

In that MoneySense post Mike explains how and why rising rates did not accompany inflation. It’s very relevant to today’s economic environment and the suggestion from Central Banks. They can control rates. Or let’s say they can attempt to control the interest rate environment. They control the overnight rate and they can buy back bonds to also control the rates of bonds on offer. It’s called yield curve control.

Only time will tell if inflation is just passing through (transitory) and if the powers that be can control rates. The bond markets might eventually have their say. If inflation is meaningful and lasting, central banks will likely have little choice but to increase rates (or allow rates to rise) in a meaningful way.

No real yield for U.S. stocks or U.S. bonds.

A ‘real yield’ means a real rate of turn after we factor in inflation. Many bond yields have been negative for quite some time. And now if we use the recent inflation spike we have a negative real earnings yield for US stocks. Crazy times. If you buy the U.S. stock market the collective companies (of the S&P 500) don’t earn you a dime after inflation.

Of course, greater earnings and lower inflation can reverse that event.

You’ll find that stock negative real yield chart in the MoneySense post.

As I’ve suggested many times, we can be cautious with the U.S. stock market, and we don’t have to own the market. From mid April, the US Dividend Aristocrats are fighting back.

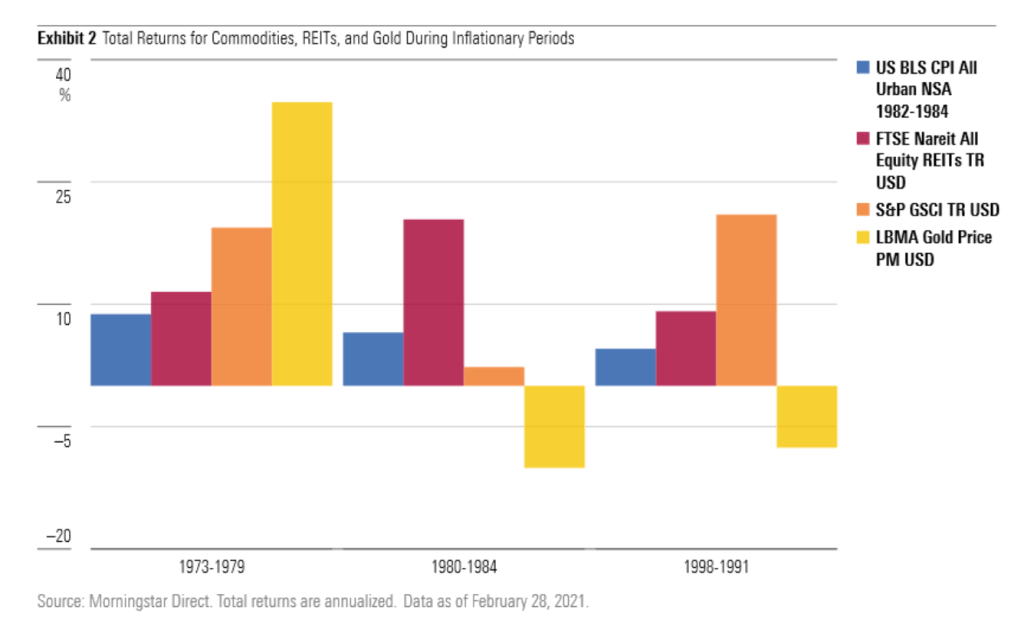

Are commodities the answer?

Here’s a very telling and important chart.

That chart suggests that a commodities basket is the most prudent approach. And of course investing in REITs is also another positive move on the diversification front.

There are options on the fixed income front as well with inflation-adjusted bond ETFs, floating rate bond ETFs and some preferred share ETFs. I am more of a fan of using types of stocks and those commodities. For quite a while I’ve suggested investing in Canadian energy stocks as an inflation hedge. I added to my iShares XEG ETF this week.

If you need to protect your wealth, I would suggest that you take a hard look at real assets and commodities.

Related post: The New Balanced Portfolio.

You might shade in a real asset ETF such as PRA from Purpose. That purpose ETF might be used in place of the Gold holdings (as it includes gold and other precious metals and base metals).

Horizons also offers commodities ETFs.

You are not in control.

Here is a wonderful post on Seeking Alpha – you are not in control.

The theme of that post is that a new paradigm has been created by the central banks, where lenders are paying many governments for the privilege of lending them money, as negative interest rates have taken hold and remain right up until this day.

If you think that the markets are operating in an uncontrolled manner, you are mistaken. The free markets that once existed, for the most part, have gone the way of the Dodo bird and into extinction.

But the author, Mark J Grant (chief global strategist at B. Riley Financial) offers that ‘they’ might get away with it all for quite some time. I’d hold the same opinion (guess).

There are those who contend that this will end soon, that it will end badly, but I am telling you – don’t hold your breath. I do not think this will end anytime soon, not for years, possibly decades, as the governments of the world cannot afford to pay higher interest rates on their debt …

I am more than happy to play the game. But it is also a dangerous game. What if governments get rates and borrowing costs that they can’t afford? What if the MMT (modern monetary theorists) are wrong, and government debt DOES matter?

Consumers might get borrowing costs that they can’t afford? Maybe inflation will be serious and lasting?

Given all of that, I will hedge with those commodities and bitcoin.

Propped up investments?

And while we’re on this ‘bearish’ theme, here’s a must-watch video featuring the bond king Jeffrey Gundlach.

https://finance.yahoo.com/video/jeffrey-gundlach-where-sees-opportunities-000506547.html

Are we investing in stocks and bonds, or government borrowing and stimulus? From that interview.

JEFFREY GUNDLACH: Well we’ve had a relationship between the Fed growing its balance sheet and the value of the S&P 500 that’s been in place for years now, ever since they started quantitative easing. And it’s almost like a law of physics. It’s like if you take the capitalization of the S&P 500 and you divide it by the Fed’s balance sheet, it looks a lot like a constant.

And yes you’ll find some investment ideas offered by Mr. Gundlach in that post. 🙂

As they say ‘you can’t fight the Fed’. Owning stocks (great companies) has been the one of the greatest wealth builders known to investor-kind. It’s right up there with real estate, earning an incredibly high salary and choosing the right parents.

Stocks are still a wonderful long term asset class if we believe in long term global economic growth. I’m a believer, and I still love our stocks. I also believe (as do many real economists) that we will return to modest or low growth and any meaningful inflation will likely be short lived. Most of the larger economic forces in play are deflationary. That said, we could get some inflationary shocks and hot spots over the next year or two.

But being in a semi-retirement stage, I can’t afford to guess about all of the above. I hedge.

Decide for yourself. But I think it’s very important that investors are aware of the current reality and the current risks and long term risks.

We’ll see you in the comment section. Are you managing the risks, or are you 100% long Modern Monetary Theory?

The inflation watch continues.

Cut your fees, support Cut The Crap Investing.

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

You will also earn a break on fees by way of many of those partnership links.

I also have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Consider Justwealth for RESP accounts. That is THE option in Canada.

At Questrade, Canadians can buy ETFs for free.

I use and I’m a big fan of the no fee Tangerine Cash Back Credit Card. We make about $55 per month in cash back on everyday spending.

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are still at 2.3%.

Kindly use the buttons below to share this post.

Dale

Thanks Dale, reading your posts is one of the best parts of my weekend (the 20+ degree weather today take top spot, unfortunately!)

I should have bought more XEG when it was under $4 last April – that was when everybody was ridiculing Eric Nuttall for his call on oil prices to rise…look who’s laughing now. My XEI has been a great play for the oil theme plus CDN dividend stocks. Like you said a number of months ago, it was built for this environment.. Cheers

That is so kind of you, thanks. I think there is much more to come from XEG and holdings. I’ll keep adding.

Thanks for the comment and thanks for stopping by.

Dale

Your prescient post suggests we are entering a “new monetary era” …. one where governments are quietly slipping in MMT and UBI. One has to wonder about the future value of any currency going forward. Like, who needs to borrow your dollars if the Fed will just print more and more every day? My grandfather experienced inflation, and currency debasement, and his advice was “never sell your Real Estate”.

Yes, real estate is one of those assets known to be a very good inflation hedge. Real assets, hard assets.

Thanks Steve.

Dale

Dale, on a very practical point and with the many unknowns and moving parts per your above post, when do/did you start extracting the cash that you’ll need for 2022? Thanks

Hi Bob, we keep a separate cash component and the portfolios are always being fed with bond and dividend income. Cash is not a great concern with the balance that we keep in stocks and bonds and some cash.

Dale

Thanks Dale. I’m new to the “retired” game and having had such a good run on the markets, I’m thinking I should pull back a little on the equity throttle. I don’t need an ever increasing portfolio value, but I do need it to be there when I’m drawing cash to cover our annual expenses.

The following has certainly not been my experience ” if we use the recent inflation spike, we have a negative real earnings yield for US stocks. Crazy times. If you buy the U.S. stock market the collective companies (of the S&P 500) don’t earn you a dime after inflation.” The problem here is in buying the collective companies of the S&P 500″.

I wrote a book in 2020 in which I provided charts of all 628 stocks on the NYSE and NASDAQ that paid dividends of 6% or more. In September of 2020 I scored each of the 628 and then sorted the 628 by score, dividend yield percent, share price and alphabetically. The book was released in December.

In February of 2021 one of its readers emailed me and marveled over how much the top scoring stocks in the charts had accelerated in value. I went back and re-scored the top 20 stocks and put the results in a chart which I will send to anyone who is interested (email imacd@informus.ca). That reader was right. Almost all the 20 share prices were up by 15% or more and paying dividends of 7% or more.

If you want to see the scoring matrix I used go to http://www.SaferBettrDividendInvesting.com. Canadian stocks were also scored

I have been scoring stocks and investing this way for the last 16 years. It has allowed me to live very well off my dividend income which generates more than 6% a year even in recessions and pandemics. While there is not a capital gain of 9% every year, most years this target of 9% is exceeded. My portfolio is now more than 3 times large than when I became a self-directed investor and still growing.

During the 2008 and 2020 recessions my share prices dropped by 40% but 95% of these financially strong companies in my portfolio continued to pay their same dividend. All I do in a recession is relax and live off the dividends and wait for the portfolio to again reach record highs as it always has.

For safe diversity and ease of handling I limit the number of stocks in the portfolio to the best 20 dividend stocks I can find. I rarely make a change to the portfolio. Most years perhaps 1 or 2 stocks, who must both score below 50 and show a dividend percent drop below 5, will be replaced with a better stock.

I suspect this way of investing only works if you are s self-directed investor. A full-service investment advisor’s fees would eat up too much of your dividend income. It is a long way from the buy cheap and sell high philosophy that speculators follow.

My background was developing commercial risk scoring systems. I just applied what I learned there to picking safe stocks that would grow and provide a reliable income. I came to recognize that investment risk is just another form of commercial risk.