The year 2021 was the first full year of the pandemic. Most of us continue to be surprised that a pandemic turned out to be the best thing that could happen to stock markets. Of course, the stock market rally has been fueled by record amounts of fiscal stimulus (government support) and low interest rates. Those low borrowing costs can stimulate the economy and speculation. That said, the earnings for U.S. and Canadian companies is real, and the stock markets took notice. It was a banner year for stocks and for simple balanced ETF portfolios. Let’s have a look at the 2021 returns for the ETF portfolios on Cut The Crap Investing.

You might start with a look at the ETF portfolio page.

An ETF portfolio will allow you to invest in the stock markets around the globe. You can manage the risks with bonds, cash, bitcoin (digital gold), gold and other commodities. Today, we’ll look at the simple core couch potato models on Cut The Crap Investing.

Be sure to check out the ultimate couch potato series that I help manage for MoneySense.

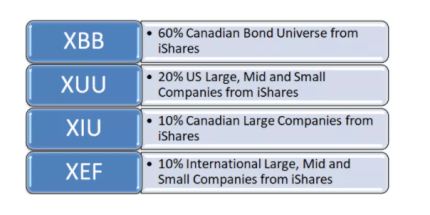

Basic couch potato core assets

You can certainly build around this core. For greater diversification and risk management have a read of the new balanced portfolio. That takes more of an all-weather portfolio approach.

Here are the portfolio models for consideration, plus the returns for 2020 and 2021. The total returns includes dividends. The following are Canadian Dollar ETF models.

More advanced investors may purchase U.S. dollar assets held in U.S. dollar RRSP accounts for greater tax efficiency. In that case, you would avoid withholding taxes on the U.S. dividends. You can also find greater tax efficiency by holding U.S. Dollar assets in U.S. non registered accounts.

The Balanced Portfolio With More Bonds

- 2020 total return 10.1%

- 2021 total return 6.9%

The Balanced Portfolio With More Stocks

- 2020 total return 10.5%

- 2021 total return 12.9%

Balanced Growth Portfolio

- 2020 total return 11.0%

- 2021 total return 17.4%

All Stock Growth Portfolio

- 2020 total return 9.8%

- 2021 total return 23.6%

The aggressive portfolios had banner years. Stocks did very well, while core bonds were in the red thanks to rising rates. I’d suggest that you don’t run away from bonds if you need to manage your risk tolerance level. Adding more bonds typically reduces the volatility in a portfolio. Bonds will usually go up when stocks get crushed. Owning bonds in the portfolio can decrease the percentage that the portfolio will fall (drawdown) in a major correction. With less of a drawdown, the portfolio can recover in quicker fashion compared to an all stock or stock heavy portfolio.

We must always invest within our risk tolerance level.

The 3-year and 5-year returns

The returns have been more than generous. Couch potato models prove that very successful investing can be very simple, and easy. Keep it simple. Keep it cheap.

If you are still in high-fee mutual funds, compare your returns to these couch potato models. Be sure to match the risk level for comparison (the stock to bond ratios).

Most Canadians will find that there is no comparison.

If we compare our balanced growth couch potato ETF model with the TD Comfort Growth Portfolio (balanced growth mutual fund), we find a vast outperformance for the ETF option.

Buy ETFs at no cost at Questrade

5-year annual returns, ETF portfolio vs TD

- Balanced growth ETF 10.8%

- TD Comfort growth 6.3%

That TD fund is a good proxy for the typical Canadian who is invested in high fee mutual funds. Those poor-performing funds often come with no advice, or poor advice.

The advantage of earning an additional 4.5% per year is astounding. It is life changing. Even over a 25-year period you’d experience returns that would be triple that of the mutual fund model. Imagine the potential of retiring with three times as much money in your RRSP and TFSA?

Yes, it is a big fat no-brainer.

If you want a managed all-in-one ETF portfolio, you can use one of the asset allocation ETFs.

If you want a low-cost ETF portfolio that comes with advice and financial planning in some cases, check out the Canadian Robo Advisors.

These are all far superior to the high-fee mutual fund approach in Canada. Make 2022 the year that you ditch your poor performing funds.

To those who are investing in a sensible low-fee manner, congrats on another very successful year of wealth building.

Thanks for reading. We’ll see you in the comment section. How was your 2021?

How to leave your high-fee funds behind in 2022

You will also earn a break on fees by way of many of these partnership links.

CANADA’S TOP-RANKED DISCOUNT BROKERAGE

Cut the Crap Investing readers can earn a break on fees at Questrade by way of that partnership link. At Questrade, you can buy ETFs for free.

I have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Here’s Canada’s top-performing Robo Advisor.

Consider Justwealth for RESP accounts. That is THE option in Canada with target date funds that adjust the risk level as the student approaches the College or University start date.

OUR SAVINGS ACCOUNTS

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are at 1.25%. You’ll find some higher rates on certain GICs. They now also offer U.S. dollar accounts. They have been awesome.

OUR CASHBACK CREDIT CARD

We make between $60 to $70 every month! And that’s on everyday spending. There are no fees with …

The Tangerine Cash Back Credit Card

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

Kindly use the buttons below to share this post.

Leave a Reply