There is no denying. By almost every measure, U.S. stocks were at historically high valuations in 2021 and especially heading into 2022. Stocks were driven higher thanks to TINA – there is no alternative (to stocks). Bonds are terrible, so buy stocks, no matter how expensive. The thing is, bonds and U.S. stocks both offer a negative real (inflation-adjusted) yield. And make that an underlying earnings yield for stocks. U.S. stocks were vulnerable to a rising rate environment. And now we have stock market corrections to the tune of 8% for the S&P 500 and over 12% for the growth-oriented Nasdaq. The big question is – when will U.S. stocks become attractive? When will U.S. stocks offer reasonable longer term value? How much farther do they have to fall?

A reliable indictor for valuations and the prospects for returns over the next several years or decade is CAPE – Cyclically Adjusted Price to Earnings. CAPE looks at the underlying earnings and smooths out the numbers over time to remove any noise.

Valuation and stock performance

At high valuations, stocks typically deliver less returns over time. While the market provides many swings and can get silly at times, earnings account for 80% of returns. From that silly post –

Valuations today are near the level of the dot-com crash of the early 2000’s. What followed was the lost decade for U.S stocks. We don’t even want to talk about what happened after 1929.

And of course, past performance does not guarantee future returns, or lack thereof.

We can’t time the market

There is no reliable way to time the market. Let’s get that out of the way first. You can’t time the market, but you can certainly control the level of earnings that you buy. You can control the level of dividend income and bond income that you buy.

Related post: Dollar cost averaging vs lump sum investing.

Insisting you always receive a reasonable amount of earnings from a company is called value investing. The greatest investor in history is Warren Buffett who operates Berkshire Hathaway (BRK and BRK.B). Warren Buffett is a value investor.

Mr. Buffett did not buy stocks in the COVID correction of 2020. He does not appear to be buying hand over fist in 2022. I will certainly keep an eye on the world’s greatest investor. I have been watching Warren from the time of this post …

You can invest like Warren Buffett, or you can invest with Warren Buffett.

I like to do a little bit of both. I pay attention to valuations, and Berkshire Hathaway is our largest individual stock holding.

When will U.S. stocks become attractive?

I’ve posed this question to contacts that I trust, and I trust that they’ll quickly offer up a helpful chart or statistical framing. Mike Philbrick of Resolve Asset Management shot back with …

On valuation The trailing P/E of 26.4 is 51% higher than the historical average trailing year P/E ratio of 17.5.

Mike Philbrick, January 26, 2022

The trailing PE ratio refers to the latest (actual) earnings reports. A forward PE is based on estimated earnings for the next year.

Given the above, we’d need to see a 34% correction to get to the historical average.

The forward PE

On Seeking Alpha (in a public exchange with me) an author who goes by the Dividend Sensei handle offered …

According to JPMorgan, stocks are 16% overvalued based on the 25-year average forward PE of 16.8. A 13% decline gets us back to historical fair value.

Dividend Sensei, January 27, 2022

What do stock prices have to say?

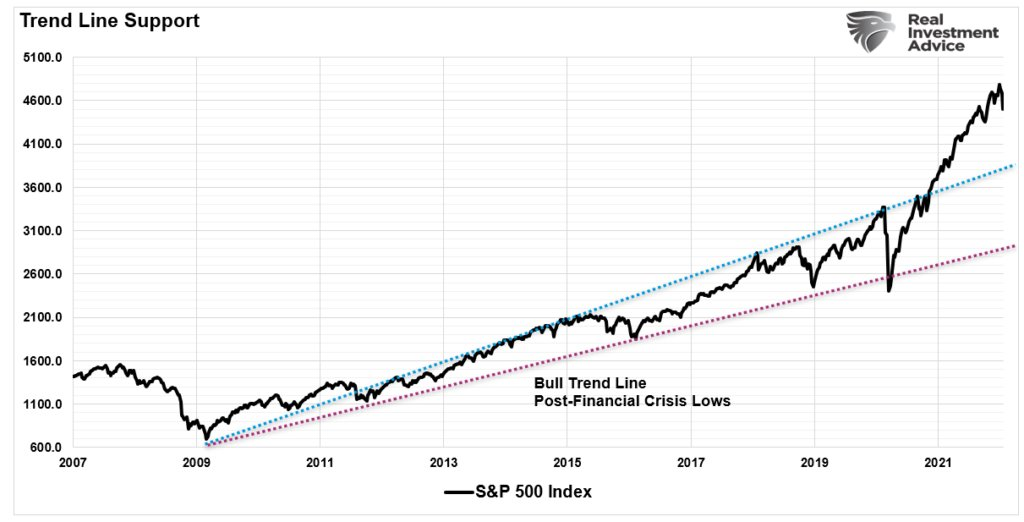

I checked in with Lance Roberts of RIA Advisors who offered this chart, from January 26, 2022.

An 18% correction in the S&P 500 takes us back to the historical bull trend line. We see that the band is measuring the top and bottom trends for stock market gains, from the great financial crisis.

An additional 52% correction takes us to the bear market trend line.

Of course an additional 52% correction is a scary thought, and that would likely bring financial chaos and ruin. Dividend Sensei offered additional context on that.

Because if stocks fall 30% to 35% too quickly, then global margin calls tighten financial conditions and the Fed has said it will do whatever it takes to prevent a financial crisis. Could stocks fall more than 35% if they did so gradually? Sure. Flatten the margin call curve and financial conditions will remain stable. And Jay Powell is on the record saying the Fed has no problem with bear markets as long as financial conditions are stable.

And here is a chart from this must-read post from our favourite economist, John Mauldin.

That chart and analysis suggests that we need a 36% correction to get back to median fair value. What a wonderful read that is. It lays out the risks in clear and sensible fashion.

And this just in from Liz Sonders of Charles Schwab …

How Powell might get lucky

Powell does have a few things going for him. The economy is relatively strong right now. As Omicron recedes, more people will come back into the workforce and fill the demand for labor. The more time Powell can buy, the better the supply chain situation gets. That will help on the inflation front. He could possibly get rates above 1% (oh, the horror!) and inflation near 3% and falling. The markets will notice the world is not ending, setting up that V-shaped recovery.

John Mauldin

Something has to give, eventually

Since 2009, the S&P 500 has averaged gains of roughly 15% a year, well above the historic returns of roughly 10% a year. Many attribute that 5 percentage point yearly outperformance all or partly to the Fed. You can add in the direct fiscal COVID support as well to businesses and individuals.

All said, 15% annual returns cannot continue indefinitely. We don’t have the economic growth to support that level of returns. Though sure, the impossible is possible.

The U.S. markets will take a breather at some point. They can correct in vigorous fashion. Markets can also offer very muted or no real returns for an extended period.

It’s the Fed vs real growth

Keep in mind, the backdrop is we do have recent economic growth and ongoing earnings growth. I cover that and more in my most recent Making Sense of the Markets column for MoneySense.

And you’ll want to read this post that frames on ongoing earnings growth story.

The threat is the valuations and the market reset as we enter a rising rate environment. TINA is getting some competition. In a rising rate environment growth stocks with low earnings multiples get repriced. We are seeing an ongoing rotation to value stocks, a theme that I have put on the table for many months. Financials and energy stocks lead the charge.

Canadian markets offer greater value and they are holding up quite well. And especially those big Canadian dividend ETFs.

Here’s a very good video with Martin Pelletier.

Martin is more of a fan of U.S. banks due to the highly leveraged nature of us Canucks. We never did deleverage coming out of the financial crisis. Americans did.

If you manage your own stock and ETF portfolio you don’t have to buy the market. You can find value in the U.S., Canada and in International markets.

You can buy value.

Your weapons in a market correction?

You don’t have to be a value investor. If you hold a core couch potato ETF portfolio regular investments and rebalancing can help to take care of any value distortions.

Of course, you might consider the new balanced portfolio.

Related post: The all-weather portfolio for retirees.

If you have an investment plan, carry on.

Add monies on a regular schedule. Rebalance as per your predetermined mandate.

I’d be more than happy if my Canadian holdings and commodities continue to do well while U.S. stocks fall.

And yes, in regards to U.S. growth stocks, I am waiting for those stocks to become attractive.

The best companies in the world

The U.S. market offers many of the best companies in the world. We might get a wonderful opportunity to add to those companies at much lower prices. If those growth stocks reverse course, and continue on to new highs, no problem. I will continue to trim and move those profits to other stocks and to risk-off assets such as bonds and cash.

Framing the growth and forward PE ratios

From Barron’s. – In aggregate, analysts expect earnings per share in the value fund to grow 10.5% for calendar year 2022, according to FactSet. That’s still better than the growth fund’s expected EPS growth of 7%. The growth fund is expected to see EPS growth average almost 12% for the two years following 2022, compared with the value fund’s average of just under 9% for that span. The aggregate forward price/earnings multiple for value has only fallen 3.2% year to date to 15.5 times. Meanwhile, the growth fund’s multiple is down 6% to 25.3 times.

Risk is different in retirement

I am in the semi retirement stage and will approach portfolio management much differently than someone who is in the accumulation stage. Those investors in the accumulation stage with many decades to go, might continue to add on a regular schedule. It is the “dollar cost averager” who will catch the market bottom. From the bottoms and near the bottoms, we often scoop up some wonderful long term gains.

Forward returns from market troughs (bottoms) after major corrections …

Thanks for reading. Please leave a comment with your ideas, concerns or questions. Or feel free to send me a note by way of that contact form.

Don’t forget to follow this blog by way of the Subscribe button.

How to leave your high-fee funds behind in 2022

Change your financial life. You can also earn a break on fees by way of many of these partnership links.

CANADA’S TOP-RANKED DISCOUNT BROKERAGE

Cut the Crap Investing readers can earn a break on fees at Questrade by way of that partnership link. At Questrade, you can buy ETFs for free.

I have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Here’s Canada’s top-performing Robo Advisor.

Consider Justwealth for RESP accounts. That is THE option in Canada with target date funds that adjust the risk level as the student approaches the College or University start date.

OUR SAVINGS ACCOUNTS

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are at 1.25%. You’ll find some higher rates on certain GICs. They now also offer U.S. dollar accounts. They have been awesome.

OUR CASHBACK CREDIT CARD

We make between $60 to $70 every month! And that’s on everyday spending. There are no fees with …

The Tangerine Cash Back Credit Card

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

Kindly use the buttons below to share this post.

Dale, thanks for posting on this topic. The implications of such a crash in equity prices raises a question that you may be able to help with: At what point would you pull from your cash wedge, cash cushion, or whatever you call it?

The scenario is, you are retired and the last two years have seen your portfolio’s value increase by 35%, this despite your bonds dropping by 10%. In the two weeks before your planned sale of stocks/equity ETFs to cover your near future living expenses requirement, global equity prices drop by 15% to 20%, and there’s a strong expectation that the price recovery is a long way off. Would now be the time to draw on your cash reserves (or sell other forms of fixed income)?

What I’m trying to understand is, at what point should we start using up our reserves of fixed income; it’s there for a reason! Thanks

I love this question and I’m really interested in Dale’s thoughts. Based on my research this is pretty much the text book case to use your cash wedge account in order to avoid selling your holdings at a depressed price.

Or, is it?

Hi Bob, I think the idea would be to have already rebalanced along the way. And that is, when you have outrageous gains in one asset, move profits to your underperforming assets (take any taxes into consideration). Also, when your stocks are doing great, you can simply harvest from those stocks, exclusively, to fund retirement. Wondering if you have been doing that for the last couple of years?

That helps do some ‘rebalancing on the go’.

These days, you might continue selling more stock if your allocation to stocks is still above your target range.

And that said, let’s connect offline and I can get you some opinions from an advisor or planner. It might also make for a nice post as well, if you’re up for that.

Dale

Hi Dale, yes, we have been re-balancing our Canadian investment accounts, in part, using dividends, and cash that we had hoped to spend on our 2020 and 2021 vacations.

For the past two years, to top-up a DB pension income, we have been withdrawing lump sums from foreign [RRSP like} pension plans. Putting cash into investments, while pulling from other investments may seem odd to some, but it’s to do with leveling our taxes during our retirement years, and also, those foreign pension plans have annual fees of 3%.

Thanks Bob. That sounds prudent to top up more pension income.

I have also sent you an email, several days ago. It might be in your spam, have a look.

Dale

Bob,

Include me in the exact scenario you laid out. I’m going through a similar thought process with an additional thought of pro-actively shifting portfolio emphasis to value rather than growth (depends where you are on the age curve).

I know .. I’m getting tempted by the “timing game”.

Hey Miles, I have responded below and I did reach out to Bob. Perhaps we can make this a test case. I could get some more help for your situation as well. There are many friends out there willing to pitch in.

Dale

Miles, I know what you mean. I’ve mostly been able to control my “timing game” urges by settling on five years worth of fixed income (cash and bonds); I hate it, and I can sleep well knowing that I have it!

From the investment and risk point of view, I focus on maintaining the five years of fixed income funds, and let the equity portion do whatever it will do. From the withdrawal perspective during a crash, I’m not so sure, and when is a crash a crash from my portfolios perspective.

Great post Dale. I think US would have to take a breather for now. Since every cycle, has a leader, since 2008, US has been taking everything along..next 2-3 years it goes sideways or gives very little gains would be just fine..in the mean time..i think Canada from relative valuation has been so neglected since 2008 would probably have a chance to shine al teast for next 2-3 years

It would be very nice if Canada could shine while the U.S. slides. I’d be more than happy to buy the best companies in the world as they go on sale. Regular rebalancing can achieves some of that as well of course. You’d have a pre-arranged rebalancing plan.

Dale