It is more than unfortunate that for two weeks running the top story in my MoneySense column is the invasion of Ukraine. Nothing is more important than the human suffering (of course). It is distressing and surreal. But given my ‘job’ I do address the economic and portfolio considerations. In this week’s post I address the inflation shock that we are all feeling from the invasion of Ukraine. The War on inflation, on the Sunday Reads.

Here’s the link to Making Sense of the Markets. From that post:

Russia is a major energy, metals and potash producer. It supplies some 41% of the natural gas imported by the EU. Russia and Ukraine are also major agricultural producers and exporters. The war is inflationary on many fronts.

I also noted that –

As central bankers attempt to battle inflation, they do so within the fog of war.

The world has changed. Risk has changed for all of us, on every front.

In the post I also wonder if bitcoin has a PR problem, and I look at the portfolio risk managers recent performance – gold, commodities and more.

Preet Banerjee looks at the sanctions applied against Russia, and answers who are Russian oligarchs?

More Sunday Reads

If you want your portfolio to participate in the green shift, here are Canada’s top renewable and clean energy stocks. Yes, you can find generous and growing profits in the sector. That post is courtesy of stocktrades.ca. I am looking to build up a position in green energy producers, over time. Perhaps I will as I sell some of my energy stocks.

Yesterday on this site I had another look at the Ninepoint Energy Income Fund that will launch on Monday. We might be in the golden era of free cash flow for energy producers.

The all-weather portfolios

Mark Seed looks and an all-weather ETF portfolio model on My Own Advisor. That is Mark’s weekend reads post.

You might also consider this all weather ETF portfolio idea on Cut The Crap Investing.

On The Findependence Hub, Jonathan Chevreau penned that the Ukraine invasion underlines investors’ need for super diversification.

On A Wealth of Common Sense, the mistaken post – there is no hedge for everything. Author Ben Carlson suggests that nothing works for ‘real’ inflation. I’m glad that Ben finally realizes that stock markets don’t work during rising inflation or stagflation. I had tweeted that fact to Ben, and for that, he blocked me, ha.

Of course commodities work. They are reliable and they react with enthusiasm. As per that Man Institute study, the only sector that works is energy. A few stock styles work as well such as Quality.

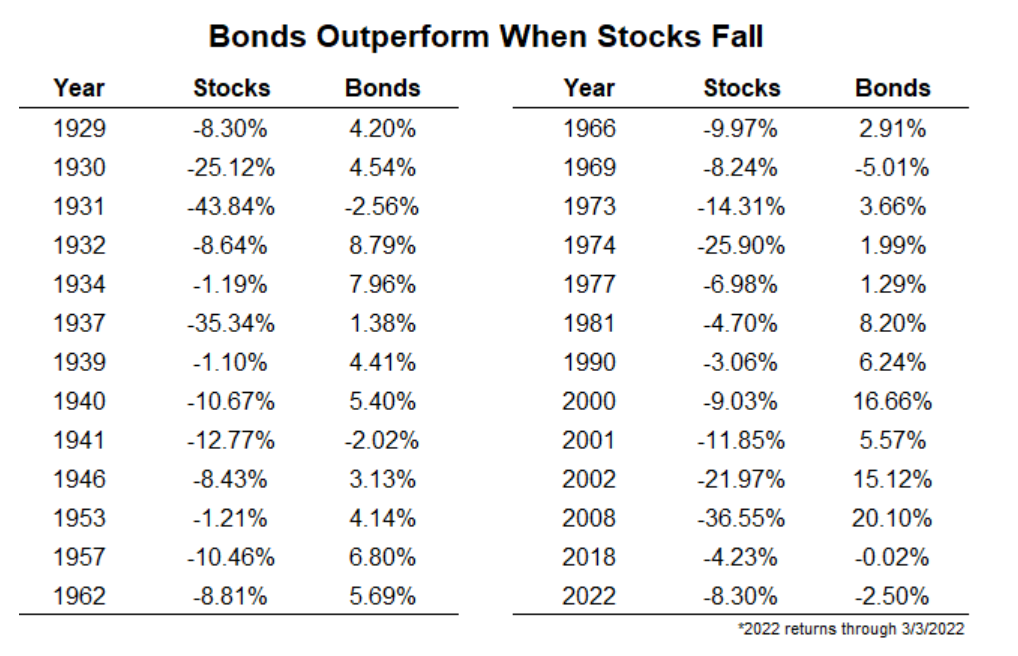

From the Wealth of Common Sense post, here’s an interesting chart on the relationship between stocks and bonds (when stocks correct).

Of course, core bond funds make for a poor inflation hedge, but they do a wonderful job of keeping an eye on the stock markets. Bonds are the adult in the room. I will also refer to bonds as portfolio shock absorbers.

A FIRE alternative

Here’s a very thoughtful post on Banker On Wheels, an alternative to the the traditional FIRE. From Belgium, Romain Tancré rode in and has joined the team. Romain offers his experience and take on Financial Independence Retire Early (FIRE).

Here is my alternative.

Instead of saving enough money to go from “Full-time job” to “Fully Retired”, target a lower savings amount, and go “Partially Retired”, working part-time on something you deem meaningful, while also pursuing asymmetric (high risk and high rewards) activities.

That is the path that I took. I’m not sure how many times I have “semi retired”.

We have the portfolio size effect on FiPhysician.

In summary, the risk is highest the day before you de-risk. The reason: portfolio size effect means that you will have to keep working (if you can) or suffer sequence of returns risk.

But the real risk is not meeting your goals in retirement. The basic idea: Get the Last Doubling, but don’t be thrown out at home plate. As your human capital decreases, it is time to take some chips off the table. In the trade-off to the last doubling vs the portfolio size effect, understand when you have won the game.

On the proper mindset for an investor, Bob at Tawcan knows that you should be an owner of great businesses.

And, as always, a wonderful weekly wrap of stock stories and blog posts of concern from Dividend Hawk. Including –

And …

There is a a big dividend and total return tally on My Prudent Life. That is a nice looking TFSA.

And Rob at Passive Canadian Income is ready with his February update.

And while Canadians love their dividends and Canadian stocks I will always ask investors to consider what is the cost of any Canadian home bias?

Helping Ukraine

More than a million people have been displaced from Ukraine since Feb. 24, and aid is urgently needed. You might consider making a contribution to the Canadian Red Cross or another charitable organization of your choice.

Other options are the Canada-Ukraine Foundation, Help Us Help, Save the Children Canada and Global Medic.

Thanks for reading, we’ll see you in the comment section.

Cut The Crap Investing Partners

You will earn a break on fees by way of many of these partnership links.

CANADA’S TOP-RANKED DISCOUNT BROKERAGE

Cut the Crap Investing readers can earn a break on fees at Questrade by way of that partnership link. At Questrade, you can buy ETFs for free.

I have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Here’s Canada’s top-performing Robo Advisor.

Consider Justwealth for RESP accounts. That is THE option in Canada with target date funds that adjust the risk level as the student approaches the College or University start date.

RETIREMENT FUNDING PLANNING

The self-directed investor might consider the service provided by Mark Seed from My Own Advisor. He runs Cashflows & Portfolios where they will provide options for that optimal retirement funding strategy. That service is provided for a very reasonable fee.

If you do head to Cashflow & Portfolios, be sure to tell them Cut The Crap Investing sent ya 🙂

OUR SAVINGS ACCOUNTS

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are at 1.25%. You’ll find some higher rates on GICs, recently updated and increased t0 2.05% for short term offerings. They also offer U.S. dollar accounts. We use them, they have been awesome.

OUR CASHBACK CREDIT CARD

We make between $60 to $70 every month! And that’s on everyday spending. There are no fees with …

The Tangerine Cash Back Credit Card

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

Kindly use the buttons below to share this post. Don’t forget to follow this blog, use that subscribe button.

The “bottom line” is that the invasion of the Ukraine is being financed by the Western Nations, that have sacrificed energy security for the United Nations zero-carbon economic suicide pact ….Welcome to a new world !

We might have a new energy reality, and yet we did not yet come to terms with the previous energy reality. I’m happy to be hedged.

Dale