Dividends are so popular. That’s an understatement. Government agencies have forced that upon us. We live in a low yield environment. Bonds come up way short in the task of delivering safer income for retirees. Naturally, investors turn to dividends. Can we live off of the dividend income?

The yield on iShares Core Universe Bond Fund XBB is about 2.8%. Not only that, the income has been decreasing.

Low income in concert with falling income is not sweet music to the ears of retirees. Bonds suck. That was the theme in should you roll the dice with your retirement savings?

In that article a financial planner argues that retirees should invest entirely in stocks. There’s greater growth potential in stocks. But with an all stock portfolio we have no protection from those nasty market corrections. The early 2000’s and the 2008 financial crisis chopped stock prices in half.

Living off of the dividends.

Dividend growth investors will offer that they can take the stock market risk out of the equation by ‘living off of the dividends’. A major risk for a retiree is called that sequence of returns risk. Selling off the stocks in a 50% off scenario in market corrections can kill the goose that laid those golden retirement eggs.

If a dividend investor generates the income that they need from the dividends there’s no need to sell the stocks in a market downturn.

Generous income and growing income.

The dividend growth investor turns the tables on that low income and falling income problem of the bonds. Stock dividends can deliver generous income and growing income. Typically you hear of dividend growth investors joyfully bragging about their 9% or 10% annual raises.

Did you get 10% annual raises when you worked?

Imagine that. You quit work but you still get a raise. Heck you get a raise that likely dwarfs the rate of salary increases you experienced when you had to battle through traffic to make it to the office. Look at Mike in that hammock. He’s lying around, collecting his ‘salary’ increases. He’s resting in that hammock but he’s living off of those dividends.

In the land of retirement funding chatter, we often talk about that 4% rule. The idea is that you might be able to start retirement by spending 4% of your portfolio value, and then allow for annual increases to account for inflation. It’s a useful benchmark but here’s why we also ignore that 4% rule.

Can you create 4% income today?

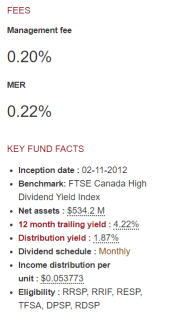

In Canada, that’s not problem. Even the Canadian high yield dividend funds are above that 4% dividend income level. For my wife’s accounts I use Vanguard’s Canadian High Yield Index Fund, ticker VDY.

We can see that the trailing yield is 4.2%. The dividend growth rate is choppy at times, but very impressive.

The first full year of operation in 2013 the fund delivered .75 cents per unit. That has increased to $1.33 per unit. That investor (aka my lovely wife) has enjoyed a raise of over 75%. Of course, that raise is just from the initial investment. I’ll write of that triple compounding that we can experience when we reinvest dividends and also add our new monies. Then, we’re really fattening up that goose.

That’s some goose. Some eggs.

The first reader who emails me with the historical figure who inspired ‘some goose, some eggs’ wins a Cut The Crap Investing coffee mug. OK, I don’t have any CTCI coffee mugs but if anyone knows the answer you’ve created a new task for me. I’ll get a hundred made and hand them out like candy.

Of course in the retirement stage when we’re simply living off of the dividends we have to rely on the fund increases in distributions or dividend growth from the stocks if we hold a portfolio of individual stocks.

Individual stock portfolios vs ETFs

For my personal RRSP account I have skimmed several holdings from the land of High Yield Canadian Dividend Payers. My income and income growth is a little better than VDY and my concentrated portfolio did not experience the dividend decline in 2016.

Here’s an income demonstration for every $10,000 invested, courtesy of portfoliovisualizer.com.

- Dale = Portfolio 1

- VDY = Portfolio 2

Certainly, I have concentration risks. I am counting on oligopolies over numbers of stocks. Don’t try this at home. Keep in mind that many advisors will also hate VDY as it is concentrated heavily in Canadian financials.

Big dividends in the U.S.A.

The comparable Vanguard fund for the US market is VYM. The yield on that fund is about 3.1%. That fund has been on a tear in regards to the price. The total returns have been generous and the dividends can’t keep up to the share price increases.

While the dividend growth over time is impressive, that fund delivered a sizable cut in distributions through the financial crisis of 2008. That’s not surprising. This is a US fund; the financial crisis was born in the USA. Many banks were generous dividend payers at the time and found their way into this index.

From 2008 it took 4 years for the income level to increase to new highs. Here’s the quarterly dividend graphic as per Seeking Alpha. Note: always double check your sources for any financial numbers, stocks and graphs.

The dividend investor might be prepared to live off of a little less. And certainly many do acknowledge the risks and accept the possibility that they may see some dividend disruption. They have replaced stock market price risk with dividend growth and health risk.

Our friend Mark Seed of myownadvisor is a dividend investor who is aware of the realities. He simply wants to put himself in a position where he does not need to sell any shares. He’ll accept some lesser income as well, if need be.

The dividend dream is alive and well.

Here’s Mark with why his goal to live off of dividends remains alive and well.

Here are some key thoughts from Mark.

- I continue to believe there are simply too many unknowns about the future. Having ample capital for our financial future will give us many options.

- If we are able to keep our capital intact we don’t need to worry as much about when to sell shares or ETF units when markets don’t cooperate.

- I don’t necessarily believe in the 4% rule – the ability to draw down your portfolio for 30 years (or so) without the worry of running out of money. It’s impossible to predict next year let alone 30 years.

- I find dividend income easy to track.

- It’s tangible money I can spend if and when I choose without worrying about stock market prices or gyrations.

- I agree with other investors – including many dividend investors – dividends seem to be more stable as part of total return than the hope of capital gains.

Caring for Clients

And here are some wonderful considerations from our friend Rona Birenbaum of Caring For Clients.

Interest in dividend equity investing has grown in popularity. There are a few driving forces behind the trend including:

- Low yields on conservative fixed income investments

- Lower taxation of eligible dividends vs. interest income

- Low cost of owning individual securities vs professionally managed equity portfolios

- Excellent performance of high quality dividend equities, ETFs, and funds and pools historically.

- Investor confidence in the strategy

A 100% dividend equity portfolio may not be optimal if:

- The dividend income is insufficient to meet cash flow needs and capital withdrawals are required. Selling equities during a bear market and subsequent recovery may undermine future growth of the portfolio and will reduce the dividend income the portfolio generates, resulting in an ever increasing need to draw on capital.

- If the investor is at risk of selling some or all of the portfolio during a bear market as a result of their stated volatility tolerance and/or their behavior in past bear markets.

- Many dividend portfolios we see are largely focused on Canadian investments. A properly diversified portfolio includes investments beyond our borders.

So will the dividends get the job done?

It’s a great strategy. Most importantly, it can help investors stay focused in the accumulation stage. It has the potential to help retirees stay the course during any market turbulence. That said it may not be all that easy to keep your eye on the dividends in a major market correction. Know thyself.

I am with Mike The Dividend Guy. While I enjoy my big juicy Canadian dividends, I feel that a dividend growth total return approach may be the most optimal. I have no problem harvesting Apple shares to take a trip or two. And quality rules. I did own VYM at one point. Research then led me to the lower income Dividend Achievers. That index fund and those companies help up much better than the S&P 500 in the Financial Crisis. The Dividend Aristocrats offered incredible stability in the last 2 major stock market corrections. I like the strategy of juicy Canadian dividends plus quality and total return potential for US holdings. I also feel it’s important to manage that sequence of returns risk.

Got dividends?

What about you? Do you have plans to live of of the dividend income? Or perhaps you’re a core couch potato investor even in retirement. That works too.

Please leave your thoughts in the comment section. Always invest within your risk tolerance level. Ensure you understand all tax implications. Consider some international equities as well. Seek qualified advice.

Dale