Unfortunately I am not talking about my own Apple stock holding. I’ve done very well with Apple, initiating a position in 2014, and adding a few times soon after. I then trimmed a few times creating homemade Apple dividends to help fund trips to PEI, starting in 2018. But my Apple holding pales in comparison to a reader who received a financial review in the Financial Post. He had way too much success with Apple stock, if that’s possible.

Of course the ‘too much success’ is a wonderful problem to have. In that Financial Post article we read that the bulk of the investor’s wealth is in that Apple stock.

Their cost was about $41,300 based on the exchange rates at the time. Today, that Apple position is worth $3,360,000 and makes up a significant chunk of their net worth of $4.4 million

Once again, that is a great problem to have. And obviously there is too much concentration risk in one company. Even if one sees that as a wonderful company with very strong long term prospects. Of course, I am biased, I see Apple as a wider moat ‘lower risk’ stock over the longer term. Apple has an incredibly strong brand and a very loyal customer base. They are diversifying away from a reliance on iPhone sales and are creating repeatable income by way of subscriptions and paid services.

What happened to disruption?

And they sit on a mountain of cash. All said, it’s only one company that operates in a sub sector with the potential of incredible disruption. Personally, I find that in recent years there has been a lack of ground-breaking disruption in the smartphone space. Companies such as Apple and their competitors are only making incremental improvements in camera or enhanced features or power. That lack of true disruption is a plus for an Apple shareholder. There’s been no biggie to knock King Apple off of its throne.

My love for Apple stock and products aside, there is stock market risk, individual stock risk, economic risk, pandemic risk, inflation risk etc. Those risks need to be managed and some Apple stock needs to be sold. The question is – how much Apple stock should be sold?

Sell all Apple and create a $1.4 million tax bill?

That appears to be the suggestion from the financial planner who is offering advice in the article. You’ll read in that article that the husband and wife (Bill and Cindy) want to buy a new home and need to raise monies for that purchase. But sell all of that stock and send the taxes to Ottawa?

Why the rush to create that immediate cash? Borrowing costs are at record lows. Bill and Cindy could get a mortgage, perhaps even at 1%. There is no absolute need to pay for that house in cash. It is a great time to be a borrower.

Sell enough Apple to protect against a market downturn.

I’m not a financial planner, but here’s my back of the napkin thinking. $390,000 of the Apple stock is in TFSA tax free savings accounts. I see those TFSA accounts as an option to sell some stock and add some diversification. Perhaps they sell $140,000 of Apple stock leaving a healthy $250,000 Apple holding. Of course it’s a tax free account, there will be no tax consequences.

That investor then might use that $140,000 to buy US and International stock ETFs, plus bonds that might include Canadian, US and International bonds. I had penned on the Vanguard Global one ticket bond ETF. I would also add some gold ‘stuff’ and bitcoin.

Canadians can hold the 3iQ bitcoin fund in a TFSA. Full disclosure, I hold that fund.

Prune that Apple tree over several years.

With respect to the non registered Apple stock holding, I would consider selling that down over several years. There’s almost $3,000,000 of Apple stock. If that investor has that longer term faith in Apple they might sell off $400,000 per year over several years and move those monies to a conservative blend of stocks and bonds. They might even consider Horizons one ticket ETFs. They are corporate class and tax efficient. Once again, I would top them up with some gold and bitcoin and cash.

Given that the investor from the article had $65,000 in unused RRSP room, the tax hit from the stock sale in year one might be in the neighborhood of $90,000, as an estimate.

The investor could then create retirement income from the TFSA account, from a portion of the Apple non registered share sale proceeds, and ongoing, from the new balanced mix in the non registered account. They have RRSP funds to draw from as well.

It’s a balance between the tax hit and the risks of stock markets and the concentration in Apple. Spreading out the Apple stock greatly reduces the tax hit, but it increases that stock market risk. That said, with a more balanced portfolio even in year one, there may be no need to sell Apple stock if it falls precipitously. The investor can wait it out, and take monies from balanced holdings in the TFSA, RRSP and non registered accounts.

What do real planners think?

Once again, I’m not a planner. That is my quick reaction to the horror of a seven figure tax bill. I will contact a few financial planners to see what they have to say. I’ll follow that up with a new post on this Apple problem. If you’re an advisor or planner and you’re reading this and want to give it a go, send me a note via that contact form.

Here was one option offered …

Would create a synthetic sale with a bank. Delay capital gains for 5 years. Get 90% of the value of stock to diversify. Easy peasy.

Stay tuned.

The Weekend Reads.

On Savvy New Canadians, Enoch has a very nice overview of investing in ETFs.

And on that subject I was more than happy to offer this co-production with our friends at Horizons – How to build the Balanced Portfolio with ETFs.

This week on MoneySense I took a look at Canadian pipelines and also a very interesting message from Elon Musk to his employees. We take a look at how the Canadian stock market is fighting back.

And here’s the weekly newsletter from The Sunday Investor. Click on Week 50. There’s an incredible compilation of graphs and charts, including …

You’ll also find the weekly breakdown of asset class returns, and returns of each stock within each sector for the Canadian market.

On findependencehub Jonathan Chevreau asks if it’s a good time for a travel and leisure ETF. A common theme that I buy into is that the pent up demand for travel and experience is incredible. That will be unleased when we get to the other side of the pandemic.

This week on My Own Advisor planner Steve Bridge stopped in to detail what a financial plan should cover.

Banker on Wheels offers a wonderful look at his around-the-world biking adventures, and draws parallels to the investing experience.

Here’s how to invest like the Ontario Teacher’s Pension Plan.

Stocktrades.ca goes against the grain and takes stock of bonds.

On Million Dollar Journey Expat Kyle Prevost takes a look at the best ETFs for Canadian Expats.

And here’s a look at the November dividend update on GenYMoney.

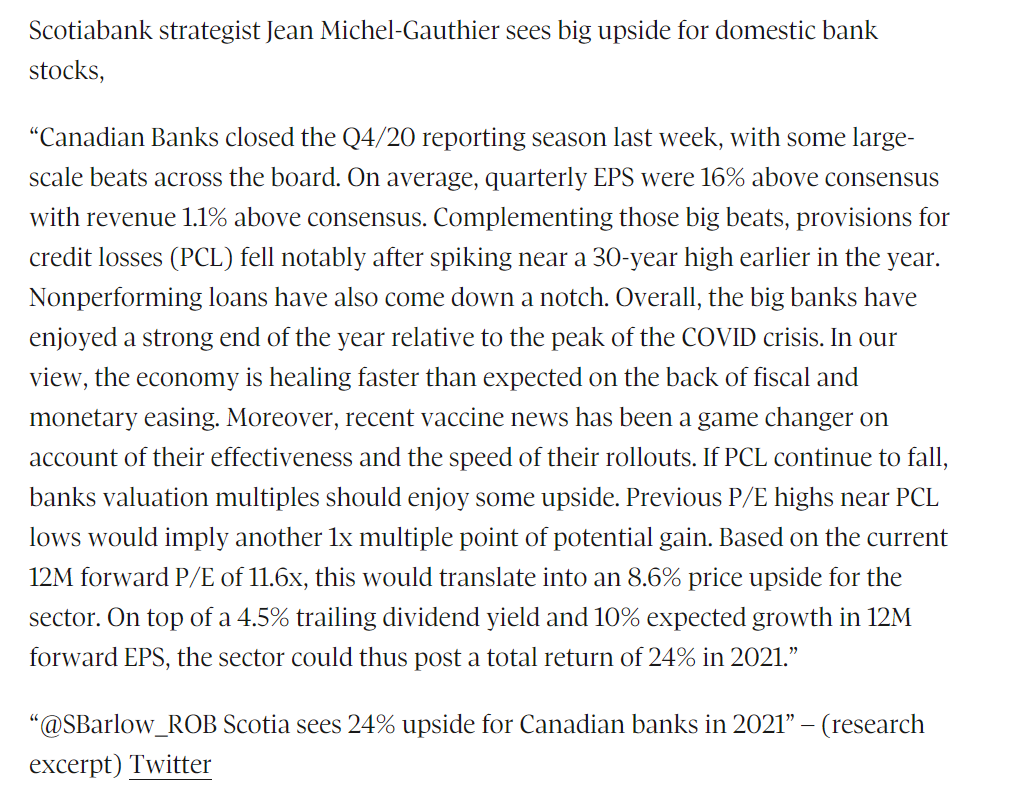

Canadian banks stocks. 24% upside?

A Tweet from Scott Barlow. I’ll take that 24%, thank you very much.

Thanks for reading. We’ll see you in the comment section. What would you do if you had more than $3,000,000 in one home run stock?

Partnership links.

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads, and hence, easy to read.

Check out EQ Bank for those who want to make their cash work a lot harder. The current high interest savings account rate is 1.5%. EQ Bank recently introduced RRSP and TFSA accounts with a rate of 2.3%. You’ll also find GICs.

I also have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple and Questwealth from Questrade.

Dale