Vanguard recently ‘disrupted’ the land of retirement funding and one ticket ETFs. They released a one ticket retirement income ETF – ticker VRIF. The new release created quite a stir. It was a hit with bloggers and the greater financial press. Many Cut The Crap Investing readers were more than interested after I posted a review. Even our US readers asked where they could find a US listed equivalent. All said, monthly income funds and ETFs are nothing new. In fact the BMO monthly income ETF has been available from 2011.

So what’s the big deal with the Vanguard one ticket VRIF ETF?

The fund will create an income stream equal to 4% of the value of the ETF that you hold. If you hold $100,000 worth of VRIF, it will pay you out $4,000 annually, in monthly installments. Have a read of my VRIF review in that link (above) for further details and specifics. It is a great option, but it is certainly not a complete retirement solution.

It’s a hit with investors as they are obviously looking for simple and reliable income producing assets. VRIF uses a total return approach to retirement funding. It will sell a portion of the stocks and bonds to create income.

The BMO Monthly Income ETF also offers a monthly income stream. But that income is derived exclusively from income producing assets. The income will ‘come from’ dividends, bond income and covered call ETFs.

I had also looked at the BMO Monthly Income ETF with investing for income in 2019.

Retirement Zoom chat and presentation.

I co-hosted a retirement-focused Zoom presentation and Zoom chat with a reader Q&A. I covererd the retirement basics, a few key considerations, plus retirement ETF portfolio construction.

Here is the link to the retirement video. Or you can click on the VW van.

Total return or income?

For retirement funding from ETFs should you look to income producing assets or from more traditional ETF model portfolios? I will leave that up to you, but I certainly understand how and why many investors prefer to use ‘real income’.

I am in the hybrid camp. My research leads me to believe (or know) that the most reliable income stream is created from a mix of some generous and reliable income, in concert with a total return stream. I use Canadian stocks for more of the generous and reliable and growing dividend income stream. Our US stocks provide a mix of growing dividends, but the real income potential will be thanks to the incredible total returns. I have created homemade dividends by selling shares.

And while the BMO Monthly Income ETF pays out a monthly distribution, it certainly fits that hybrid model. At the core are Canadian, U.S. and International dividend growth stocks. I really like the current positioning of those BMO dividend ETFs that you’ll find in ZMI.

Additional retirement risk management

I also manage the stock market risks by way of Canadian and US bonds, as well as gold, commodities and Canadian energy stocks. I also hold Bitcoin at a near 5% weighting.

Investors might consider a healthy cash component as well.

That said, a VRIF or BMO’s monthly income ETF, ZMI might be a piece of the puzzle for many investors and advisors.

ETF assets and weightings for ZMI

Weights for 2019.

Here is an updated asset mix graphic. January 2022.

In my opinion the ETF offers a sensible mix with that obvious slant to income producing assets. The current yield available in early 2022 is 3.8% .

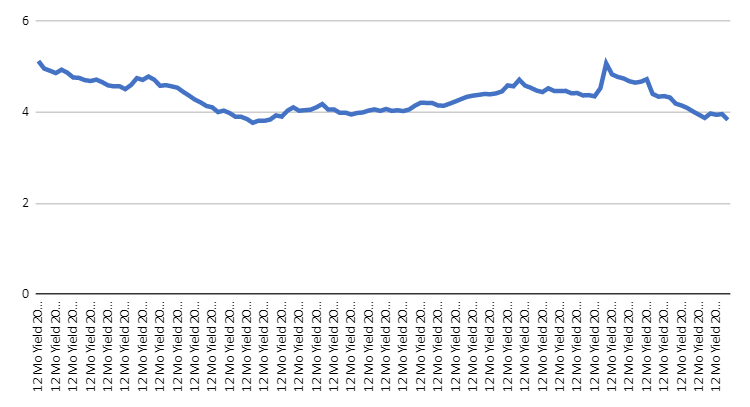

And what about that yield history for ZMI? Here’s a chart courtesy of our friends from BMO ETFs …

We can see that the initial yield for the fund was an impressive 6%. It dipped below the 4% annual range in 2014 and into 2016. Of course the yield available at any time is affected by the share price for the ETF. For a period where the distribution remains constant, lower share prices will offer a greater current yield.

Here’s an updated current income chart to January of 2022. Thanks to increasing share prices, the current yield available has slipped. But that is a good problem to have. A retiree can also sell shares to create retirement income.

Also, from the earlier years, an investor in the ETF would have seen an income reduction. But recently we see some income stability. The ETF has been paying out .06 cents per unit from 2018. The first payment in 2022 is also .06 cents. Keep in mind that neither the BMO Monthly Income ETF or Vanguard VRIF offer a guarantee of increasing income, or even stable income.

For those in the accumulation stage, here’s the total return chart for ZMI.

And the calendar year performance. The BMO Monthly Income ETF delivered a total return of 11.14% in 2021.

Retiring with BMO’s Monthly Income ETF

Here’s a hypothetical 4.8% spend rate from inception. A $1 million portfolio would deliver $48,000 in annual income before taxes, at the end of the period the portfolio balance is $1,023,731. There is an annual inflation adjustment of 2% to 2.5%.

Retirement funding is not that difficult (or tricky) during robust bull market runs.

If we move into more of a pronounced stock market correction I like the chances of the dividend growth approach vs core equity market funds. But of course, in meaningful and long corrections most stock funds are going to fall. There is usually nowhere to hide.

The BMO Monthly Income ETF has no hedge against severe stock market declines. Corporate bonds can act more like stocks, the preferred shares are stock and bond hybrids. Given that most retirees are conservative you might also hold a significant cash bucket. How much is a personal call and will depend upon your greater retirement financial plan.

The cash bucket

You may hold 2 years of spending needs in cash, you might hold enough cash to cover several years. And how much you need to dip into that cash bucket will depend upon how well your income from ZMI holds up. Your cash will be used to top up that ZMI income. You might use short term bond ETFs and short term bond ladder ETFs as well within that cash bucket.

And while stocks can be a solid inflation hedge at times. There are periods when stocks are not successful inflation fighters. You might consider adding some commodities or an all-in-one ETF such as the Purpose Real Asset ETF, ticker PRA.

If you were to build around the BMO Monthly Income ETF it might look something like …

- BMO Monthly Income 70%

- Cash bucket 20%

- Purpose PRA 10%.

If you want to go more conservative, bump up that cash position.

The above is not advice. File it under ‘ideas for consideration’.

Cashflows & Portfolios

Of course, it is also very important to develop a retirement spending plan that is tax efficient. We also need a plan that offers the most optimal order of asset harvesting, from RRIF, TFSA, non registered, pensions and other sources of income.

You might check in with Cashflows & Portfolios. That is operated by Mark Seed, who you know from My Own Advisor. The founder of Million Dollar Journey is also a partner in that venture. They will run the numbers for you. That is a very good resource for the self-directed investor.

Be sure to tell them Dale sent ya. 🙂

The income and total return combo

You might be well served to pay attention to tax efficiency for monies in taxable accounts. The total return approach may be more suitable. And as always on the retirement planning front you may touch base with a fee-for-service financial planner. Retirement funding is often more than complicated and often requires the help of a specialist.

And for tax efficiency requirements, you might consider Horizons Balanced one ticket ETF – HBAL. There are no distributions, hence not tax on any portfolio income. Of course you would sell shares as required to create income.

How about you? Total returns, or income for retirement funding? Or perhaps you opt for a mix – that hybrid option? Please fire away in the comment section.

BMO’s discount brokerage

On that BMO theme Cut The Crap Investing readers can sign up for BMO InvestorLine through this link.

And of course BMO also offers their own line up of one ticket portfolios.

To make your cash work a lot harder have a look at EQ Bank.

While I do not accept monies for feature blogs please click here on the mission and ‘how I might get paid’ disclosures. Those affiliate partnerships help me pay the bills for this site.

Kindly share this post with the buttons shown below.

Dale

I’m in the income for retirement funding camp.

I always liked the idea of BMO ZMI but never bought it because 1) it has been stuck at $100 million invested in it for years and its been around awhile 2) the MER is pretty high 3) it is concentrated in Canada and the US and 4) as much as I like my prefs and covered call ETF’s for income I didn’t want them in a all-in-one income fund.

Having said that if it got more popular I would buy it as it’s price doesn’t fluctuate much, it pays well and I like the idea of having just one fund in one of my accounts.

Thanks for sharing Dale, I didn’t know about this ETF. For sure, this ETF could be good for retirement. I choose PDC + XDIV ETFS for my differents portfolios for extra income monthly actually.

Thanks, yes there are many options for income. And of course, even that total returns approach by way of VRIF. Many routes.

Dale

Does ZMI earn its distrubations? or is it ROC ? kind of important information left out.

Thanks Bruce, the distributions are from real organic income. I thought that might have been clear in the post, but I will check to ensure. Thanks for that heads up and thanks for stopping by.

Dale

If you go to the distributions page for any ETF at its provider’s website you can see or download the distributions. ZMI has been running 19% of distributions from ROC from 2011-2019 and more recently has been running 24% from 2015-2019. That would have me worry about future capital gains from ACB.

Vanguard’s yields tend to be lower because they make much less use of ROC.

Dale, it would be great if you could do a post or point us to something that compares the life-cycle of a strategy with high ROC and eventual larger ACB capital gains vs. taking less yield and ROC, with less ACB capital gains.

I will have a look, thanks.

Dale

Hi Bart, et al, the ROC of capital is what we might call good ROC. It is due to new investors coming on board. The organic income level is then shared with new shareholders. New monies added to the fund can be used to supplement that income, but it is only at the level of the real and organic income from the ETF assets. This event would not occur if the number of unit holders remained constant.

And this was the reply from BMO …

“ETFs cannot pay ROC the way mutual funds do, as ETFs can only pay out what they earn, nothing above and beyond that.

In ZMI’s case, the ROC comes from fund growth. We pay out based on underlying yields. When ETFs grow, the earned income gets spread across more unitholders. We like to call this good ROC, as it results in tax efficiency without running down invested capital.”

I hope that helps. I’ll check with BMO friends to make sure I worded my bit on this correctly.

Thanks, Dale

Great post Dale. Follows nicely into my comparison question on RBF1660 and VRIF.

Another nice thing about ZMI, is the recent lowering of its Mer to .2%. All good choices in their own way. With some Big Bank brokerages soon to be implementing fees for purchasing mutual funds, ETF purchases at no cost at some brokerages will be compelling.

Keep up the timely and informative posts AL

I like the mix of high yield super SWANs like ENB and PPL and very solid dividend players like BCE & Telus. But also I realize that all income focus is a bit shortsighted so I have a very large percentage in Canadian banks. What I don’t have much is any growth and I honestly am a bit mystified about how to make money on US stocks. It’s the exchange on the currency that looks like a signficant risk of diminishing returns through the currency conversion on both buying and selling. Any thoughts on that Dale?

TFSA, RRIF OR non registered?

This is our year to draw income from our investments. ZMI sounds like it could contribute. My question on any new investment is where is the fund best held for tax efficiency? We each hold ZWA in our RRIFs and I am at a loss if it best to move units to our non-registered or TFSA. Dale, thanks for your efforts, enjoyable reads.

Hi Catherine, check in with Mark at Cashflows & Portfolios, that’s exactly what they do for self-directed investors. And let them know I sent ya, 🙂

Please feel free to send me a note as well. I’d be happy to have a quick look at your geographic and asset allocation.

Dale