It was an incredible year. We experienced the first modern day pandemic and the stock markets delivered very impressive returns. Of course those market returns were fueled by record stimulus from central banks around the world. Governments pitched in with more than generous support programs for workers and businesses. In the end, we saw generous returns for the core Cut The Crap Investing ETF portfolios.

Now keep in mind that the ETF Portfolios are not a recommendation. The ETF portfolios might be a starting point to build around, or a framework for consideration. With any asset allocation we apply our own biases (bets) and ideas. There is no such thing as completely passive investing. And we all should create the portfolio that aligns with our very specific goals and that master financial plan.

If you need that plan, you might check in with a fee-for-service financial planner.

That said the core portfolios would not get you into trouble, at least not yet. 🙂 But they certainly include my bias to US stocks over International. And I’m happy to (what many would consider) overweight Canadian stocks.

And keep in mind that the portfolios do not include additional risk managers such as gold ‘stuff’, additional commodities and foreign bonds. There are no emerging market stocks or real estate (REITs), but those are wonderful portfolio additions.

I am also investing in bitcoin. I will leave any portfolio shaping up to you.

For more context, you might consider the new balanced portfolio.

Cut The Crap Portfolio Returns.

OK, let’s get to the good stuff – the ETF portfolio returns for 2020.

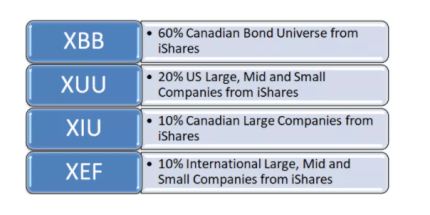

Here are the building blocks for a core portfolio.

Here are the returns for 2020, for the core assets. All were in positive territory.

- Canadian Bonds (XBB) 8.57%

- Canadian Stocks (XIU) 5.45%

- US Stocks (XUU) 16.54%

- International Stocks (XEF) 6.49%

And here are the portfolios, they are rebalanced quarterly.

The Balanced Portfolio With More Bonds

2020 total return 10.1%

The Balanced Portfolio With More Stocks

2020 total return 10.5%

Balanced Growth Portfolio

2020 total return 11.0%

All Stock Growth Portfolio

2020 total return 9.8%

Greater Growth Stock Portfolio

2020 total return 7.8%

We can see that the greater growth portfolio was not so great in 2020. It underperformed the core growth portfolio. RSP equal weights the S&P 500 constituents and that meant less of the US tech giants that drove the US market returns in 2020. And while mid cap is a long term market-beating index or approach. We did not have the beat in 2020. The Nasdaq 100 certainly offers that big US tech, but that exposure was not enough to life that portfolio approach.

As for XDIV when we looked at the Canadian Dividend ETF performance for 2020 we discussed how dividends were out of favour in 2020.

The comparative scorecard.

It was a great year for the simple couch potato approach.

The four asset approach is also employed by the Tangerine Core Portfolios. Here’s …

The Tangerine portfolio performance for 2020.

From that post here is the summary of returns for the Tangerine Portfolios for 2020.

We can see that you might have enjoyed better returns by creating your own ETF portfolio. The Tangerine core portfolios have fees (MER) of 1.07%. The portfolios equal weight the US, Canadian and International stocks. Both of those events will lessen the returns in comparison to the Cut The Crap Investing ETF portfolios.

The TD e-series funds.

Courtesy of an update on Canadian Couch Potato, here’s the returns for 2020 if you had constructed and rebalanced your own TD e-series portfolio.

There are so many wonderful low fee options available for Canadians.

For managed ETF portfolios and advice you might also consider one of the Canadian robo advisors.

And of course if you’re comfortable pressing that button and purchasing an ETF you can buy an all-in-one ETF portfolio for about .20%-.25% in fees. Recently I looked at the one ticket asset allocation ETF performance for 2020.

There are so many ways to leave your high fee mutual funds.

Thanks for reading, we’ll see you in the comment section. How did your returns stack up for 2020?

I’ll be back soon with a look at the dividend and income ETF portfolios.

Cut your fees, support Cut The Crap Investing.

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

You will also earn a break on fees by way of many of those affiliate links.

I also have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Consider Justwealth for RESP accounts. That is THE option in Canada.

At Questrade, Canadians can buy ETFs for free.

I use and I’m a big fan of the no fee Tangerine Cash Back Credit Card. We make about $55 per month in cash back on everyday spending.

Check out EQ Bank for those who want to make their cash work a lot harder. The current high interest savings account rate is 1.5%. EQ Bank recently introduced RRSP and TFSA accounts with a rate of 2.3%. You’ll also find GICs.

Dale

Can you comment on whether in the coming year or so, allocations to bonds should be reduced/replaced given the prospect of rising interest rates?

Hi Alan, fantastic question. No one knows for sure what will happen over the near term or mid term or long term with rates and yields. I am a fan first and foremost to use bonds to manage the risk of stocks and that disinflationary economic environment. So that may mean more mid term and long term bonds, and even Treasuries and more specifically US Treasuries. Stuff that might get hurt bad in a rising rate environment.

But then we have portfolio assets to help on the other side – more inflationary that might include rising rates. One might adjust their bond mix if they feel that is not properly addressed. One might shade in shorter term bonds, a shorter laddered offering, floating rate (see Horizons perhaps) or even real return or TIPS. But don’t give up entirely on your longer term bonds for managing stock market risk IMHO.

That said you might be using other assets to manage an inflationary environment and what might be a rising rate environment. And that could include gold and commodities and bitcoin and certain kinds of stocks such as energy, consumer discretionary, technology and perhaps financials.

It’s about preparing for the risks of why rates are rising – the economic environment. It’s about the total portfolio.

Hope that helps, please feel to fire away again.

I can call in reinforcements as well.

Dale

Hope this is not a dumb question, but what is the difference in buying “hedged units” of an index fund vs. “unhedged units” ?