The ‘Classic’ Balanced Portfolio offers very attractive growth potential with lower risks compared to an all-stock portfolio. The Classic asset allocation for a Balanced Portfolio is 60% stocks and 40% bonds. It is also common to see 50/50 stock to bond allocation models.

On the ETF Model Portfolio page you will see the full range of investment styles and risk levels of portfolio models. Here are those core portfolio building blocks.

Of course a Balanced Portfolio will include that bond component. Those bonds are present to add some income (not much these days), and to mostly manage the risk of those more unpredictable stock markets. Once again, if the stocks are the unruly kids, the bonds are the adult in the room.

The down-the-middle Balanced approach is the most common investment style embraced by investors for good reasons; most cannot ‘handle’ the risks associated with an all-stock portfolio. Keep in mind that the all-stock portfolios have been essentially cut in half twice in the last 20 years.

Here’s the updated returns for the core ETF portfolios.

Here’s the US Market, represented by the S&P 500, from January of 2000 to end of 2004. The chart is courtesy of portfoliovisualizer.com, and as always, past performance does not guarantee future returns.

Here’s the US Market from 2007 to end of 2011.

Here’s the US Market from 2007 to end of 2011.

That level of risk or volatility is not every investor’s cup of tea. So most investors will add bonds for support. Keep in mind that the US stock market has done very well over time but it is these severe market corrections that can shake off investors.

That level of risk or volatility is not every investor’s cup of tea. So most investors will add bonds for support. Keep in mind that the US stock market has done very well over time but it is these severe market corrections that can shake off investors.

Here’s the US market from January of 2000 until the end of September 2018. Of course we want to hop on that investment ride to grab those solid stock market gains, the key question is ‘can we hold on’ during those severe market corrections? Most investors need some support; those bonds that work like shock absorbers.

So what happens to that stock market risk when we add 40% bonds? That balanced portfolio might only see a 20%-25% drop in value when those stock markets drop in that 40-50% range. It’s more than important to invest within your risk tolerance level. It’s about understanding your tolerance for risk and then matching the portfolio to that risk level so that you can stay the course through all of the stock market ups and downs. When considering the Balanced Portfolio model you might ask and answer the question “Am I comfortable with a portfolio that might drop 20-25% in a major stock market correction”. If the answer is yes, you might consider the Classic Balanced Portfolio.

So what happens to that stock market risk when we add 40% bonds? That balanced portfolio might only see a 20%-25% drop in value when those stock markets drop in that 40-50% range. It’s more than important to invest within your risk tolerance level. It’s about understanding your tolerance for risk and then matching the portfolio to that risk level so that you can stay the course through all of the stock market ups and downs. When considering the Balanced Portfolio model you might ask and answer the question “Am I comfortable with a portfolio that might drop 20-25% in a major stock market correction”. If the answer is yes, you might consider the Classic Balanced Portfolio.

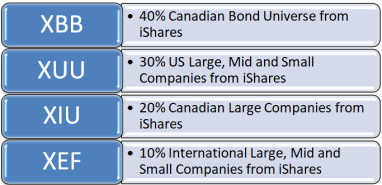

Here’s the asset allocation model ‘suggested’ or offered for consideration on the ETF Model Portfolio page. The Balanced Portfolio With More Bonds …

Using index benchmarks here’s how that Balanced Portfolio would have performed through the last major stock market correction of 2008-2009. The period is January of 2007 through to end of September 2018. The portfolio is rebalanced on an annual schedule back to original asset weightings.

We see a much ‘smoother’ ride. The worst year for the portfolio, in 2008, the portfolio model would have declined by nearly 19%. And with a hypothetical $10,000 starting portfolio value in 2007, the investor would have seen the value drop to $7,775. And that’s how one might frame the risk question. For the potential of those greater longer term gains, am I comfortable watching $100,000 potentially fall to $77,750? Am I comfortable watching $1,000,000 fall to $775,500?

We see a much ‘smoother’ ride. The worst year for the portfolio, in 2008, the portfolio model would have declined by nearly 19%. And with a hypothetical $10,000 starting portfolio value in 2007, the investor would have seen the value drop to $7,775. And that’s how one might frame the risk question. For the potential of those greater longer term gains, am I comfortable watching $100,000 potentially fall to $77,750? Am I comfortable watching $1,000,000 fall to $775,500?

On the risk front we might also ‘test’ your patience. The above portfolio model was in decline from November of 2007 to February of 2009, a period of 16 months. It then took 18 months for the portfolio to get back to even. The portfolio was ‘under water’ for 3 years.

Keep in mind that recovery periods can vary as much as the weather. The stock market correction of 2000-2003 saw US stocks under water for 3 years running. And each stock market correction is unique, they are all snowflakes. The average stock market correction over the last 70 years is more in the area of 35%, but the last 2 corrections have been doozies. We have to prepare for those events.

The Balanced Portfolio Scorecard

So here’s the scorecard for that Balanced Portfolio With More Bonds, from January of 2007 to end of September 2018. Once again, this is an approximation and each stock market correction and recovery will offer its own characteristics.

Annual Return 5.9% (CAGR)

Worst Year (- 19%)

Time Under Water – 3 years.

Cut your fees, get some offers here …

While I do not accept monies for feature blog posts please click here on the mission and ‘how I might get paid’ disclosures. Affiliate partnerships help me pay the bills for this site. That will allow me to keep this site free of ads and easy to read.

You will also earn a break on fees by way of many of those partnership links.

Canada’s top-ranked discount brokerage

Cut the Crap Investing readers can earn a break on fees at Questrade by way of that partnership link.

Here’s Canada’s top-performing Robo Advisor.

I have partnerships with several of the leading Canadian Robo Advisors such as Justwealth, BMO Smartfolio ,Wealthsimple, Nest Wealth and Questwealth from Questrade.

Consider Justwealth for RESP accounts. That is THE option in Canada with target date funds that adjust the risk level as the student approaches the College or University start date.

Our savings accounts

Make your cash work a lot harder at EQ Bank. RRSP and TFSA account savings rates are at 1.25%. You’ll find some higher rates on certain GICs. They now also offer U.S. dollar accounts. They have been awesome.

Our cashback credit card

We make between $60 to $70 every month! And that’s on everyday spending. There are no fees with …

The Tangerine Cash Back Credit Card

Kindly use the buttons below to share this post

Leave a Reply